The September Edition

By Jianing Wu

August was marked by crosscurrents across macro and digital asset markets.

In traditional markets, investors grappled with mixed inflation signals, softening labor data, and growing expectations that the Federal Reserve will begin cutting rates in September. Earlier in the month, the consumer price index (CPI) came in cooler than expected but was offset by a hotter reading of the producer price index (PPI). By month-end, the Fed meeting in Jackson Hole, Wyo., brought a dovish tilt from Chair Jerome Powell, who highlighted a “shifting balance of risks” tied to rising unemployment, reinforcing the sense that monetary policy is shifting toward easing. Equities churned but ended in positive territory, with the S&P 500 swinging on data releases, while defensive assets like gold outperformed into month-end.

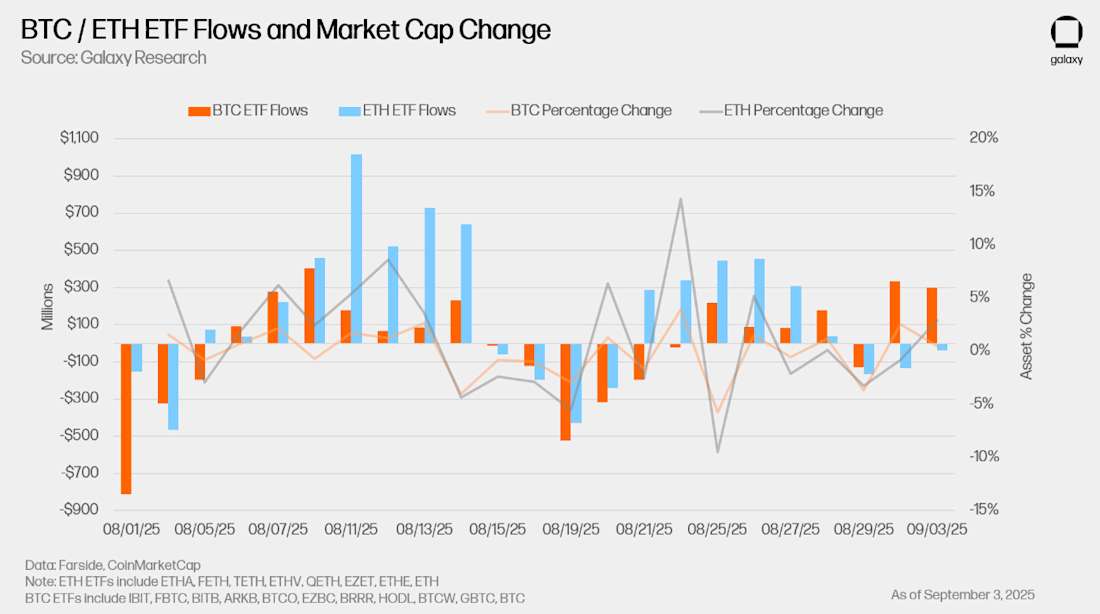

Crypto markets reflected this macro uncertainty with heightened volatility. BTC hit a fresh all-time high above $124,000 in mid-August before retreating toward $110,000, while ETH outpaced BTC throughout the month. ETH exchange-traded funds (ETFs) attracted strong inflows early on, right after seeing one of their largest daily outflows on record, even briefly outpacing BTC products despite ETH’s smaller market cap.

Still, renewed demand pushed ETH to new highs near $4,953, lifting the ETH/BTC ratio to 0.04 for the first time since November 2024. The ebb and flow of ETF activity highlighted how institutional positioning is increasingly shaping crypto price action, with ETH emerging as a clear leader in this phase of the cycle.

On the policy front, regulators made incremental moves to reshape the landscape. The U.S. Labor Department opened the door to crypto allocations in 401(k) plans, while the Securities and Exchange Commission (SEC) clarified that certain liquid staking arrangements are not securities.

Structural and institutional adoption trends deepened further. Treasury Secretary Scott Bessent revealed that the Strategic Bitcoin Reserve holds between 120,000–170,000 BTC, providing the first glimpse into the government’s cumulative digital asset holdings. Corporate activity accelerated as well: stablecoin issuers Stripe and Circle announced plans for their own L1 blockchains, Wyoming became the first state to launch a dollar-backed stablecoin, and Google entered the corporate blockchain race with its Universal Ledger. Meanwhile, digital asset treasury companies (DATCOs) continued accumulating assets.

Overall, August reinforced two key dynamics. On the one hand, macro volatility and policy uncertainty drove sharp swings in equities and crypto. On the other, the underlying trend of institutionalization accelerated, from ETF flows to sovereign and corporate adoption. These crosscurrents may remain central as markets head into the fall, with the Fed’s policy pivot and ongoing structural demand likely to set the tone for the next stage of the cycle.

001 Surges, Breakouts, and Reversals

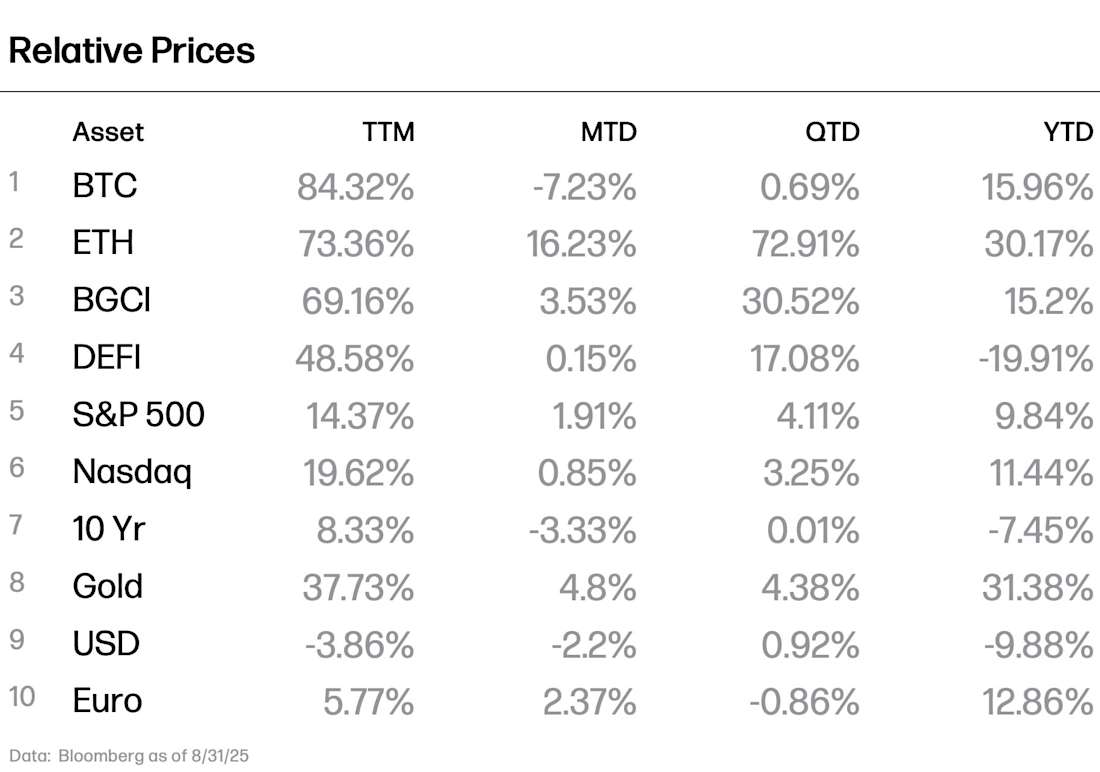

ETH led the market higher in the first half of August, outpacing BTC and driving a broad rally in altcoins, measured by the Bloomberg Galaxy Crypto Index (BGCI). On Aug. 13, BTC hit a new all-time high of $124,496 before reversing and ending the month at $109,127, below its starting level of $116,491. A week later, ETH broke through its previous cycle ceiling on Aug. 22, reaching $4,953 and surpassing the November 2021 high of $4,866, ending a four-year consolidation.

ETH’s strength was particularly notable given its underperformance for much of this cycle. Since bottoming near $1,400 in April, ETH has more than tripled in price, propelled by strong ETF flows and purchases by DATCOs. U.S. spot ETH ETFs logged roughly $4 billion in net inflows during August, their second-strongest month after July, compared to net outflows of roughly $639 million from U.S. spot BTC ETFs.

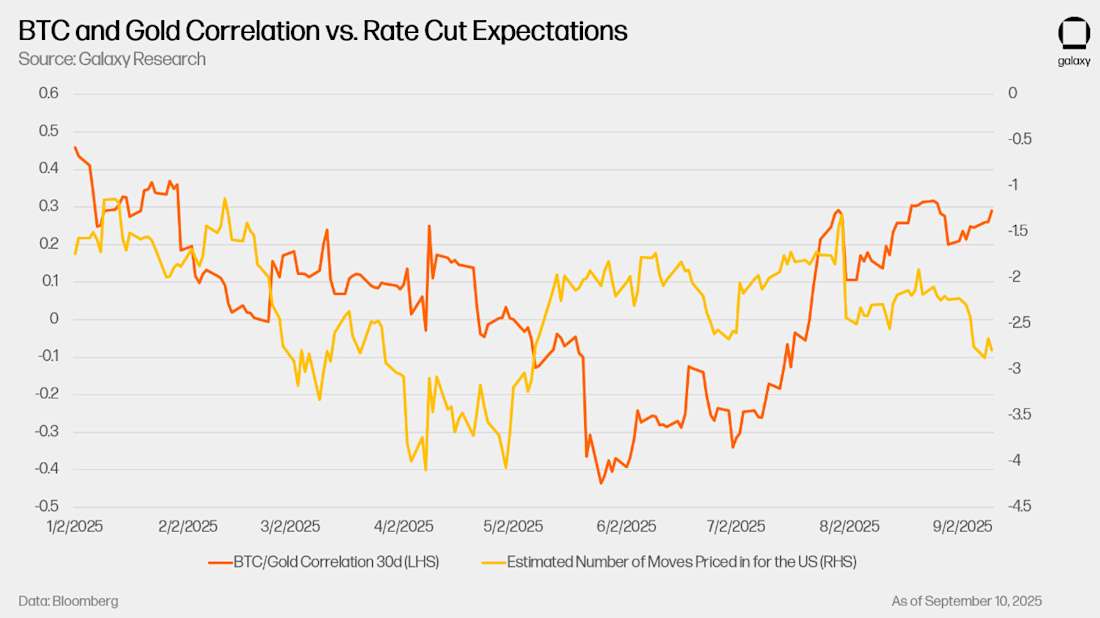

However, BTC ETF flows turned positive even though spot prices slipped in the last two weeks of August. Growing expectations for aggressive Fed rate cuts brought the store-of-value narrative back into focus, with BTC’s correlation to gold strengthening through the month as rate cuts appeared more likely.

Beyond ETFs, DATCOs remain an important source of demand. These firms continued to accumulate throughout August, with ETH-focused DATCOs in particular injecting meaningful capital. Because ETH is a smaller asset than BTC, inflows from treasury companies make an outsized impact on the spot price. A $1 billion allocation to ETH can materially shift market dynamics in a way that the same allocation to BTC cannot. Moreover, much of the announced DATCO capital has yet to be deployed, suggesting further tailwinds ahead.

During the month, total crypto market cap climbed to a record $4.2 trillion, showing how deeply digital assets are tied to broader market dynamics. Rising rate cut expectations boosted risk appetite across equities and crypto, while ETF inflows and corporate treasury accumulation provided direct fuel for BTC’s and ETH’s rallies to new highs. Even as volatility set in late in the month, the interplay of macro easing, institutional flows, and treasury demand kept crypto markets central to the risk-asset narrative.

002 Corporates Launch Their Own L1s

For more details on these stories, see our past coverage by Lucas Techyan and Zack Porkorny. Subscribe here to receive future updates.

Regulatory momentum is giving corporates more confidence to build directly in crypto markets. In late July, SEC Chair Paul Atkins announced the formation of Project Crypto, which seeks to enable equities, bonds, and other instruments to be issued and traded onchain, a step toward aligning traditional market infrastructure with blockchain technology. With this encouragement, corporates are now moving beyond using existing blockchains and launching their own layer-1 (L1) networks.

In August, three large firms announced new L1s. Circle introducedArc, a network compatible with the Ethereum Virtual Machine (EVM), with the company’s USDC stablecoin as the native gas token. Arc includes compliance and privacy features, a built-in FX engine for onchain settlement, and will start with a permissioned validator set. Stripe revealed Tempo, another EVM-compatible chain designed for stablecoin payments and enterprise adoption, following the company’s acquisitions of Bridge (a stablecoin infrastructure provider) and Privy (a crypto wallet provider). Google announced Google Cloud Universal Ledger (GCUL), a private permissioned chain focused on payments and asset issuance. GCUL would support Python-based smart contracts and already counts CME Group as a pilot partner.

The logic for building corporate blockchains comes down to value capture, control, and design. By owning the base layer, companies like Circle avoid paying network fees to third parties and can directly monetize transaction activity. Stripe can more tightly integrate a proprietary blockchain with its payments stack and can build features for customers without relying on another chain’s governance. Both see control as essential for compliance, particularly as regulators increase scrutiny on illicit finance. Choosing to build an L1, rather than a Layer-2 (L2), avoids dependence on another chain for settlement or consensus.

The reaction from crypto-native communities has been mixed. Many see projects like Arc and GCUL as borrowing technical standards from existing L1s but delivering subpar designs while excluding ETH and other native assets. Critics argue that permissioned validators and corporate-controlled governance weaken decentralization and user sovereignty. These debates echo the failed wave of “enterprise blockchains” in the mid-2010s, which struggled to attract real users.

Even with skepticism, the corporate moves are significant. Stripe processes more than $1 trillion in payments each year and holds about 17% of the global payments processing market. If Tempo delivers lower costs or better developer tools, competitors may need to follow. Google’s entry signals that large technology firms see blockchains as the next layer of financial infrastructure. The impact could be substantial if these companies bring their scale, distribution, and regulatory relationships to bear.

Aside from corporates launching their own L1s, other developments reinforce the shift of activities moving onchain. U.S. Commerce Secretary Howard Lutnick announced that GDP data will be published on public blockchains through oracle networks Chainlink and Pyth. Galaxy tokenized its own shares to test secondary trading onchain. These moves show that corporates and governments are starting to embed blockchains into core financial and data infrastructure, even as debates continue over the right balance between compliance and decentralization.

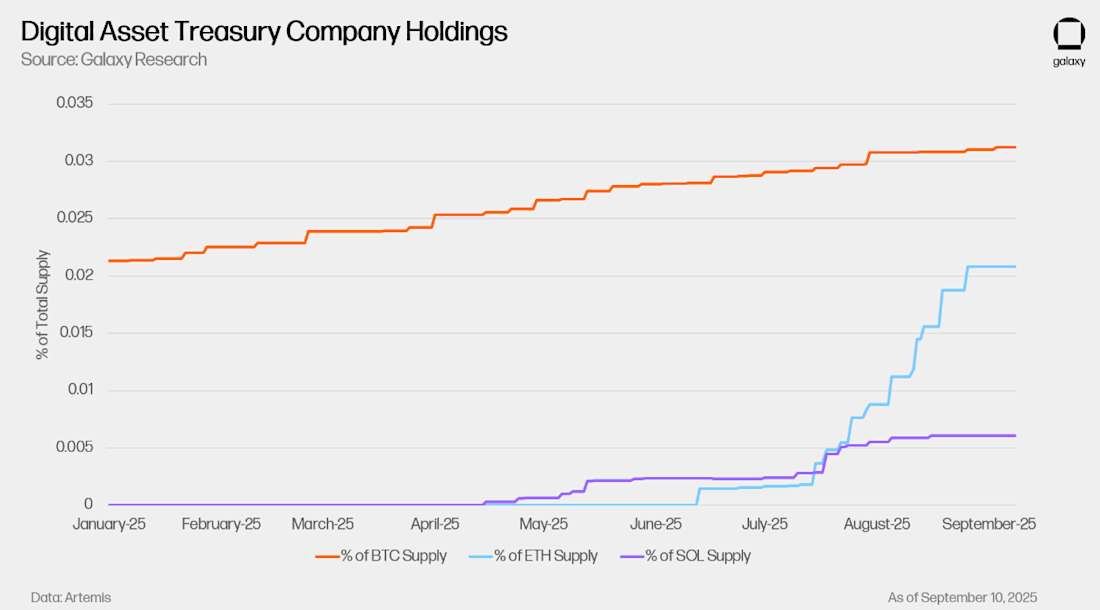

003 Persistent Trends: DATCOs

The DATCO trend we highlighted in earlier reports is still playing out. Accumulation has continued across BTC, ETH, and SOL treasuries, with ETH standing out. Holdings data show ETH DATCOs ramping sharply through August, led by Bitmine’s purchases, which grew from roughly 625,000 ETH in early August to over 2.0 million now. SOL treasury positions have also steadily increased, while BTC treasuries continue their slower but consistent build-up.

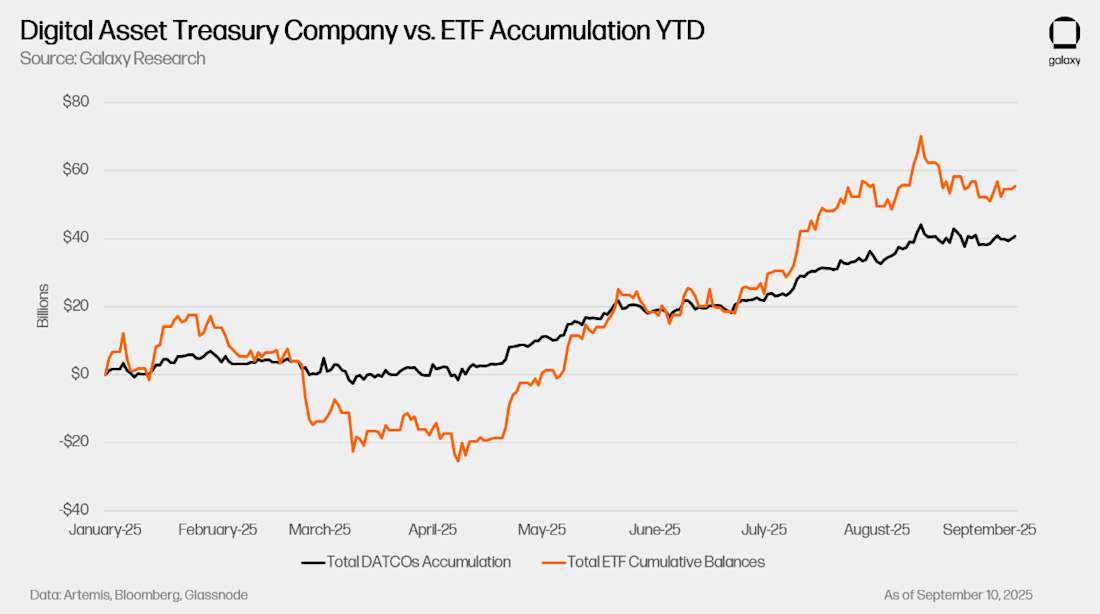

When compared with ETF flows, DATCO activity looks modest. July and August saw stronger inflows from ETFs than from DATCOs, with cumulative ETF balances pulling ahead of DATCO accumulation.

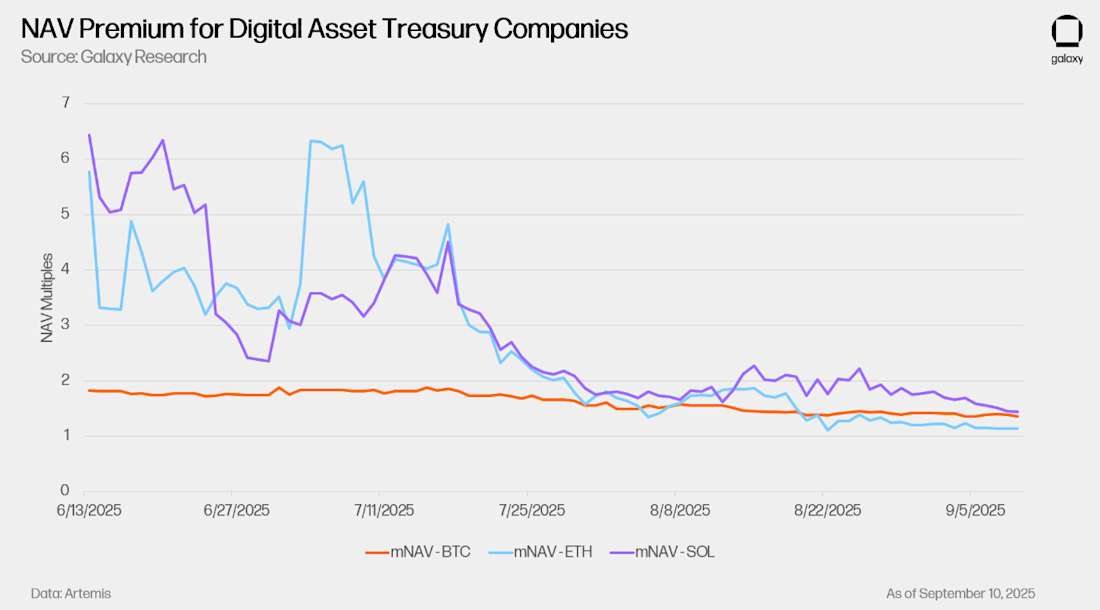

This divergence is becoming more visible as premiums for DATCO stocks have compressed across the board. Where earlier this summer DATCOs traded at multiples well above their net asset value, premiums have drifted down toward parity, signaling more caution from equity investors. That shift is visible in share prices: KindlyMD (parent of Nakamoto) has fallen to about $5 from its late May peak near $25, while Bitmine has slipped from $62 in early August to around $46.

Price pressure grew more visible in late August after reports that Nasdaq may tighten oversight of firms issuing stock to acquire cryptocurrency. The headlines accelerated selling in ETH-focused treasuries. BTC-focused firms such as Strategy (formerly MicroStrategy, ticker: MSTR) were less affected, because their acquisition strategies rely more on debt financing than equity issuance.

004 Persistent Trends: Altszn

The other trend still playing out is altcoin rotation. BTC dominance has drifted lower, falling from roughly 60% at the start of August to 56.5% by month-end. ETH’s share of the market rose from 11.7% to 13.6%. The data suggests capital rotation out of BTC and into ETH and other cryptos, consistent with the outperformance in ETH ETFs and DATCO flows. While BTC ETF inflows have rebounded [MH1] in the past few weeks, the broader takeaway remains the same: this cycle continues to broaden beyond BTC, with ETH and altcoins capturing incremental market share.

005 Our Takeaways and Predictions

Markets head into the final weeks of September with all eyes on the Fed. A weakening labor market has shifted expectations firmly toward near-term rate cuts, and risk assets have responded with renewed strength. The jobs reports underscore that the slowdown may be deeper than initially reported, raising the question of just how much easing will be required to cushion the economy.

At the same time, the long end of the yield curve is signaling caution. Elevated 10- and 30-year yields reflect concerns that inflation may remain sticky and that fiscal pressures could eventually require money creation to finance debt and spending. Short-term rate expectations are fueling the rally in risk assets, but the push and pull between near-term cuts supporting markets and longer-term concerns keeping yields and precious metals elevated could determine how sustainable the rally is. For crypto, this tension matters directly: BTC has been tracking gold more closely as a store-of-value hedge, while ETH and altcoins remain more sensitive to shifts in broader risk appetite.

Key Events to Watch:

September 17: Fed Chair Powell Speech

Key Macroeconomic Data Releases:

September 16: Retail Sales MoM

September 17: FOMC Rate Decision

September 23: Flash (Preliminary) Manufacturing PMI, Flash Services PMI

September 24: New Home Sales

September 25: Final GDP QoQ

September 26: Core PCE Price Index

September 30: JOLTS Job Openings

To learn more about the topics covered in this month's newsletter, contact our team or reach out to your Galaxy representative.

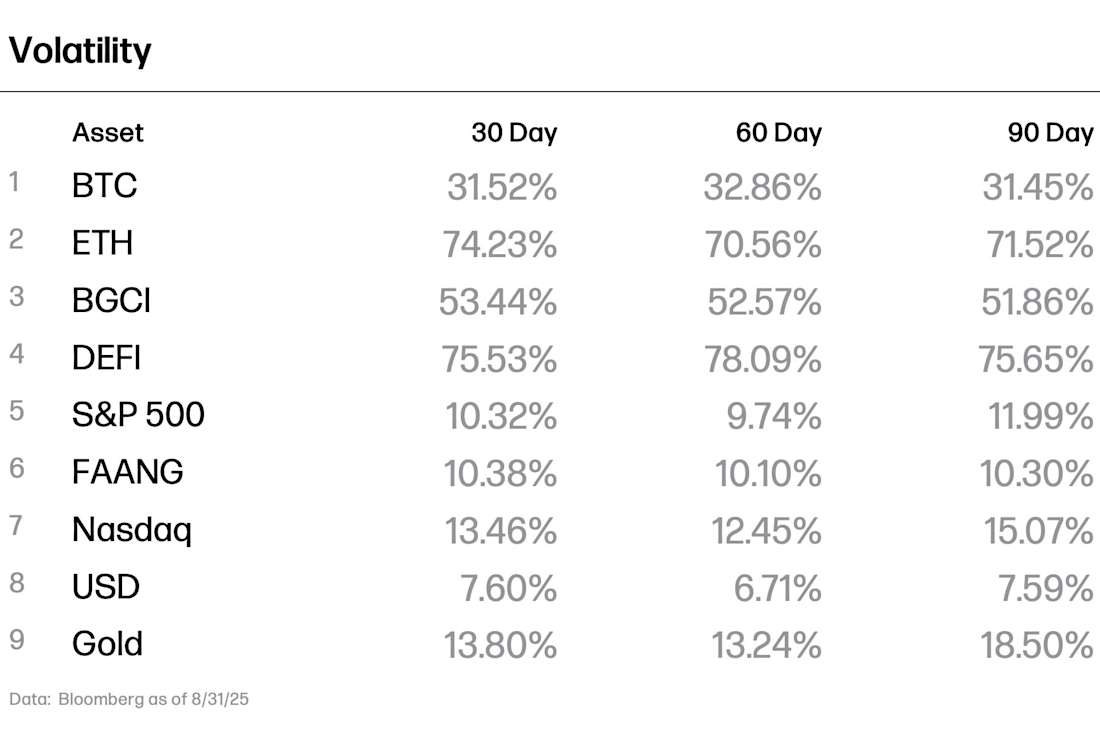

Crypto Performance & Volatility Data