The August Edition

By Jianing Wu & Su Young Lee

Markets spent July navigating a high-stakes recalibration. Fiscal expansion, shifting macroeconomic data, and crypto regulatory breakthroughs forced investors to rethink risk across traditional and digital assets. U.S. equities rallied through the month on strong tech earnings and softer inflation, but momentum faltered in the last week.

President Trump’s $3.3 trillion fiscal package, signed into law on July 4, marked the most aggressive U.S. spending plan in years. The One Big Beautiful Bill Act accelerated a drift toward deficit-driven reflation, pushing Treasury yields higher and sending the dollar to a 9.5% year-to-date decline as of August 7, the time of writing.

Early in July, there were signs of progress on trade, as the Financial Times reported that the U.S. aimed to finalize several agreements ahead of the July 9 tariff expiration deadline and Treasury Secretary Bessent indicated that multiple deals were expected by Labor Day. However, the situation quickly escalated in the second week of July when President Trump announced new tariffs on 14 countries, reigniting trade tensions. By month-end, a partial reset with Japan, featuring reduced tariffs and a $550 billion investment pledge, helped ease immediate concerns, though more uncertainty is likely to cloud the outlook.

Amid these crosscurrents, the macro data proved uneven. Headline GDP growth rebounded to 3% in Q2, but beneath the surface domestic demand softened meaningfully. Consumer spending and business investment slowed, while July’s nonfarm payroll report showed labor market gains weakening to their lowest post-pandemic pace. Markets moved to price in two rate cuts by year-end.

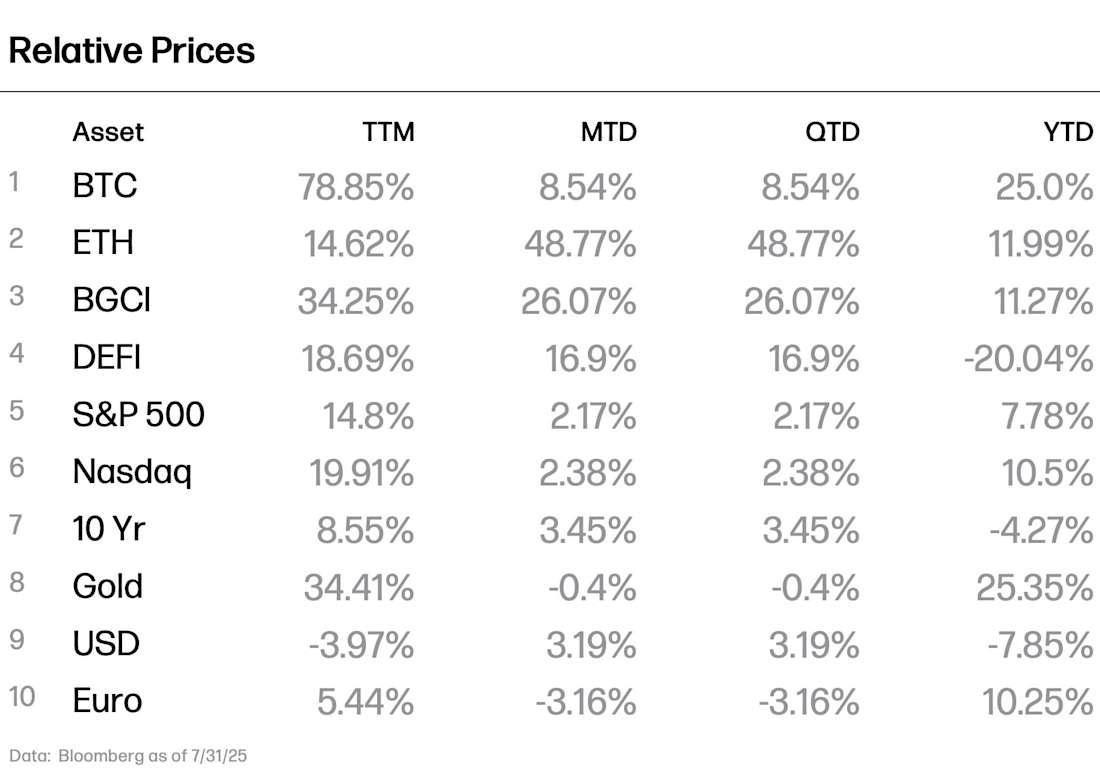

In crypto, the backdrop proved more decisively constructive. ETH led digital assets higher, rising 49% on the month as ETH treasury demand soared, U.S. spot ETFs posted historic inflows, and institutional positioning shifted in favor of yield-bearing assets. BTC achieved an all-time high with a low realized volatility, buoyed by persistent inflows and growing adoption as a macro hedge, especially against the backdrop of a weak USD and an increase in the money supply.

July also brought some of the most consequential regulatory actions in crypto’s history. The White House released a 166-page policy blueprint outlining America’s ambitions to become the global hub for digital finance. Congress passed the long-awaited GENIUS Act, and the SEC approved in-kind creations and redemptions for spot crypto ETFs. Combined with a wave of expansionary fiscal policy and increasingly mixed macroeconomic signals, these breakthroughs are fueling a capital rotation into crypto.

The DATCO Flywheel Continues to Fly: Digital asset treasury companies (DATCOs) expand beyond BTC into ETH, SOL, and altcoins.

Big Beautiful Crypto Policy Month: U.S. crypto policy saw landmark breakthroughs in July, with major legislation passed, stablecoins greenlit, and regulators laying the groundwork for a more TradFi-integrated digital asset economy.

Alt Szn? ETH outperformed in July, but the broader market has yet to show the defining signs of a true altcoin season.

001 The DATCO Flywheel Continues to Fly

Last month, we talked about the rise of DATCOs. This month, the pace of activity has only intensified. DATCOs have accumulated 96,686 BTC and 624,400 ETH in July, representing approximately $11 billion and $2.2 billion in value respectively, accounting for roughly 12% and 41% of total holdings for each crypto.

What we observed this month is that crypto treasury companies are moving beyond BTC, increasingly adding yield-generating assets including ETH and SOL, as well as selected altcoins.

ETH has become the asset of choice for many of these firms, not only due to its stature in the ecosystem but because of its ability to generate on-chain yield. SharpLink, the largest DATCO for ETH, added over 249,600 ETH in July. Bit Digital and BitMine Immersion also expanded their ETH holdings significantly, with the former holding a position of more than 120,000 ETH and the latter 300,660 ETH.

While ETH continues to see strong buying interest, SOL is also gaining traction. Compared to ETH, SOL offers a higher native yield of 7% to 8%, dwarfing ETH’s 2% to 3% yields. For crypto-native firms, holding SOL also reinforces alignment with the networks they build on and serve. For example, DeFi Dev Corp, the first and the largest DATCO holding SOL, is partnering with Solflare to offer its onchain financial products utilizing Solflare’s wallet capabilities.

The goal of any treasury strategy is ultimately to maximize returns whether through price appreciation, yield generation, or increasingly, onchain incentives, such as providing liquidity to decentralized exchanges or lending protocols. In that context, companies are beginning to explore opportunities beyond BTC and ETH, accumulating altcoins with the hope of unlocking higher ROI through more dynamic means, particularly among firms with closer ties to the coin’s ecosystem. Altcoins could serve as potential tools for earning onchain yield and forming deeper engagement with emerging networks through liquidity provisioning and ecosystem incentive programs. These moves are still relatively small in scale but demonstrate growing experimentation with protocol-native assets as flexible working capital tools, especially in DeFi contexts.

With this momentum, DATCOs continue to trade at substantial premiums to net asset value, suggesting strong investor demand for public market access to crypto exposure. That said, this growth is not without risk. Equity dilution has been substantial. BitMine, for example, increased its share count 13-fold in pursuit of ETH.

Looking forward, we expect treasury activity to deepen and diversify as the space gets crowded and current growth rates become harder to sustain. Asset allocations will likely continue rotating toward yield-generating positions. Companies investing in native tokens may accelerate the use of those assets onchain, reinforcing protocol alignment while minimizing dilution. In an environment where capital is increasingly scarce and investors are growing impatient, treasury strategies are becoming more tactical, more capital-efficient, and more onchain.

For more details on DATCOs, you can read here for a broad overview, here for a study of Ethereum DATCOs, and a primer on DATCOs’ NAV premiums.

002 Big Beautiful Crypto Policy Month

Six months after President Trump took office, several long-awaited developments advanced meaningfully across Congress. The week of July 14, which House leadership called “Crypto Week,” marked a breakthrough moment where long-simmering policy efforts finally came to fruition.

The House passed three major bills reflecting a growing political alignment around the need for comprehensive digital asset legislation.

GENIUS Act: Passed House (308–122), previously cleared Senate (68–30), signed into law by President Trump on July 18.

CLARITY Act: Passed House (294–134) but faces a complex path in the Senate. The bill touches on the interests of various stakeholders and has drawn opposition from Democrats, particularly around provisions related to the Trump family’s involvement in the industry.

Anti-CBDC Surveillance Act: Narrowly passed House (218–210), following intense debate. It now awaits Senate consideration.

The passage of the GENIUS Act provided an important step toward clarifying the regulatory framework for stablecoins. Large traditional financial institutions, which had largely remained on the sidelines, are now preparing to launch their own stablecoins. These new entrants could redefine the U.S. payments landscape by introducing more efficient, lower-cost alternatives to card networks, particularly in the credit segment, where processing fees remain high. At the same time, crypto-native firms are deepening their integration with traditional markets. Ethena Labs’ recent partnership with Anchorage to issue its native stablecoin is one such example of how distribution is evolving under a more formal regulatory regime.

As stablecoin regulations became codified, ETH gained 25.05% during the “Crypto Week,” with market participants increasingly viewing Ethereum as the institutional foundation layer for stablecoins, as approximately 52% of all stablecoin supply currently resides on Ethereum- though crypto markets remain volatile and reactive to a range of macro and policy factors.

At the end of the month, the White House released the 166-page report, “Strengthening American Leadership in Digital Financial Technology,” from the President’s Working Group on Digital Asset Markets, chaired by David Sacks. The report, ordered under the President’s first executive action on crypto, is the product of a six-month policy review and touches on topics including market structure, banking, payments, taxation, and includes a dedicated page (though little in the way of new detail_ on the Strategic Bitcoin Reserve. Galaxy Head of Firmwide Research Alex Thorn noted that “the quality, scope, and specificity of the report make it possibly the most comprehensive and decisive crypto policy document ever created by any major government.”

Regulatory momentum also continued at the Securities and Exchange Commission (SEC). The agency approved in-kind creation and redemption for crypto ETFs, aligning them with broader ETF market practices. While most crypto ETFs trade with relatively tight spreads, the decision stands to improve structural efficiency and could benefit future ETF approvals, particularly for altcoins. In parallel, Chair Paul Atkins announced the formation of Project Crypto, an SEC initiative focused on tokenization. The project seeks to enable equities, bonds, and other instruments to be issued and traded onchain. This represents a meaningful step toward aligning traditional market infrastructure with blockchain technology.

Just last week, President Trump signed an executive order allowing 401(k) retirement plans to include allocations to crypto, gold, and private market assets. Further action is likely in the months ahead. Senator Cynthia Lummis released a draft bill on July 3 proposing broad crypto tax reforms. Representative Tom Emmer reintroduced the Blockchain Regulatory Certainty Act, which seeks to clarify that developers and non-custodial service providers are not money transmitters. Neither of these bills has been brought to a vote, but both are considered priorities in the current Congressional session.

After years of delays and regulatory overhang, these events mark a period of tangible progress. Stablecoins are entering the financial system and traditional finance is preparing to operate onchain. And the legal foundation for a more integrated digital asset economy is finally being laid.

003 Alt Szn?

BTC rallied to a new all-time high of $123,000 while ETH posted a 49% gain in July. This broad-based strength was underpinned by growing regulatory clarity and institutional adoption.

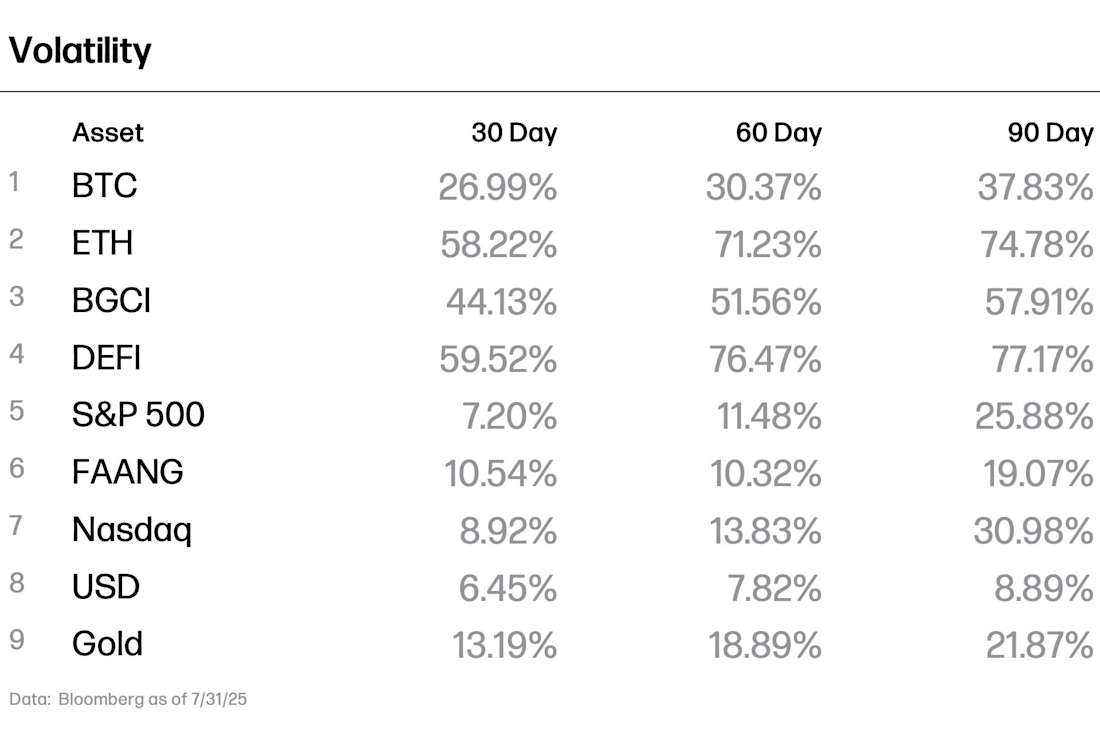

The most notable test of market resilience came in the form of a significant BTC supply event: the sale of approximately 80,000 BTC (roughly $9 billion). Despite the magnitude of the sale, the market absorbed the supply with minimal disruption, a departure from historical precedent where such events would typically trigger sharp sell-offs. Notably, this exit occurred without a spike in realized volatility. BTC’s short- and long-term volatility measures continued to decline throughout the month, with its 90-day realized volatility now lower than that of the Nasdaq 100. This trend reflects Bitcoin’s ongoing transition toward a macro-resilient asset class, increasingly uncorrelated with traditional market stressors.

Signs of structural maturity are also visible in network-level activity. The pace of BTC wallet creation has moderated relative to previous rallies. While some interpret this as a decline in organic growth or onchain participation, it may instead reflect the evolving nature of investor access. New entrants to the market are increasingly using regulated instruments such as ETFs via old-school brokerage accounts rather than creating native wallets.

The ETH/BTC ratio rose from 0.022 in early July to 0.032 by month-end, highlighting ETH’s relative outperformance. This rise was supported by $5.5 billion in monthly net inflows into U.S spot ETH ETFs. The third and fourth weeks of July also saw the two largest weekly inflows, coinciding with the first anniversary of the ETFs’ launch. When looking at onchain metrics, unlike BTC, ETH saw broad strength as its price increased, including growth in new and active addresses as well as transaction volume. These metrics suggest continued organic activity on the network, reinforcing its utility-led value proposition.

The current market cycle has yet to exhibit full-scale alt season characteristics. The Bloomberg Galaxy Crypto Index (BGCI) returned 26% in July, exceeding BTC’s 8% gain but falling short of ETH’s sharp 49% rally. This suggests that ETH’s outperformance was more idiosyncratic than indicative of the arrival of an altcoin season.

004 Our Takeaways and Predictions

Over the past two decades, July has typically been the strongest month of the year for the S&P 500, often followed by a reversal in August. This lines up with trends in U.S. equity long/short fund positioning, where net leverage typically falls sharply after July, suggesting that seasonality could once again rear its head.

At the same time, expectations for a more dovish monetary policy path are building as the labor market shows signs of strain. Last Friday’s jobs report triggered a sharp repricing in rate expectations, with markets now anticipating 2.5 cuts by year-end, up from 1.3. A softening Institute of Supply Management (ISM) Manufacturing Purchasing Managers Index adds to the case for easing.

Meanwhile, trade tensions are beginning to bite. This week, the U.S. imposed a 25% tariff on imports from India in response to its purchases of Russian oil. Imported chips and semiconductors are now facing a 100% tariff, unless companies localize production in the U.S. All eyes are on August 12, the deadline for Trump administration’s decisions on China tariffs.

Key Events to Watch:

August 21: Jackson Hole Economic Policy Symposium

Key Macroeconomic Data Releases:

August 12: CPI

August 14: PPI

To learn more about the topics covered in this month's newsletter, contact our team or reach out to your Galaxy representative.

Crypto Performance & Volatility Data