The July Edition

By Jianing Wu & Zack Pokorny

June brought trade uncertainty, geopolitical conflict, and mixed economic data. Yet, despite the challenging backdrop, risk assets rallied across the board. U.S. equities finished the month higher, with both the Nasdaq 100 and the S&P 500 setting new all-time highs. BTC briefly dipped below $100,000 mid-month but rebounded strongly into month-end, finishing up 2.84%. In contrast, the broader crypto market posted a moderate decline of 2.03%. ETH underperformed major peers, falling 2.41% on elevated volatility.

The first half of the month leaned more positive than negative, as markets digested a mix of macro data and geopolitical developments with a constructive tilt. U.S.-China trade tensions initially re-emerged but softened after a conciliatory call between Presidents Trump and Xi. China’s manufacturing Purchasing Managers Index dropped to its lowest level since 2022, and the Organization for Economic Co-operation and Development once again downgraded its global growth forecast. In the U.S., economic signals were mixed: non-farm payrolls beat expectations, the unemployment rate held steady, and jobless claims surprised to the downside, yet retail sales softened. The June CPI print marked a second downside surprise, supporting the view that inflation is cooling. The Fed left rates unchanged at its June FOMC meeting for the fourth straight time, citing a need for further clarity on inflation and labor trends.

Crypto markets navigated several short-term shocks, including a public clash between President Trump and Elon Musk over tax policy and a temporary spike in geopolitical tensions. Prices were pressured in the second-to-last week of June, but BTC rebounded alongside improving sentiment and growing institutional participation. ETF inflows into BTC totaled more than $4 billion over the month. ETH, by contrast, saw higher volatility and deeper drawdowns, though the precise driver remains unclear. Meanwhile, crypto treasury activity gained momentum, with several firms expanding their holdings beyond BTC into assets like ETH, SOL, BNB, and HYPE, reflecting the popularity of the strategy.

Geopolitics took center stage in the latter half of the month with the outbreak of the Israel–Iran war on June 13. Markets were initially unshaken by Israeli airstrikes on Iranian nuclear sites and Iran’s retaliatory missile fire. However, with the U.S. conducting strikes on three Iranian nuclear facilities on June 21, crypto prices dropped significantly, while equities held steady. Trump announced a ceasefire on June 24, brokered with Qatari assistance, easing some immediate concerns. Although sporadic missile fire continued, crypto markets largely recovered after the ceasefire, while traditional safe havens like gold and crude oil retreated, signaling reduced expectations for prolonged disruption.

The Treasury Trade Heats Up: 53 crypto treasury companies are in business, with allocations spanning eight different coins.

Accelerated Demand for Stablecoin: Following the passage of the GENIUS Act in the Senate, corporates are lining up to launch their own stablecoins.

12 Days That Shook the World (Markets, Not So Much): The Israel–Iran conflict created global headlines but had limited lasting impact on risk assets, which ended the month in positive territory.

001 The Treasury Trade Heats Up

One of the more unexpected trends this year has been the rapid rise in corporate adoption of crypto treasury strategies. The trend intensified in June, with the number of participating companies nearly doubling. In terms of volume, purchases of bitcoin by treasury companies in June exceeded the total net inflows into U.S. spot BTC ETFs, which amounted to $4 billion for the month.

While BTC and ETH remain the dominant holdings, many treasury companies have expanded into a broader set of crypto assets. Allocations now include SOL, BNB, TRX, and HYPE, reflecting growing diversification beyond the largest tokens. According to Galaxy Research, there are currently 53 identified crypto treasury companies: 36 are focused on BTC; five on SOL; three on XRP; two each on ETH, BNB, and HYPE; and one each on TRX, FET, and a general altcoin portfolio.

We expect to see the crypto treasury meta continue given the momentum of existing companies and the market’s seemingly strong appetite to fund them in considerable size and across multiple assets.

Skepticism continues to mount as more and more crypto treasury companies come online. The primary concern rests on a funding source that fuels a portion of the buys: debt. Some companies are relying on borrowed funds, largely zero-coupon and low-interest convertible notes, to purchase treasury assets. Upon maturity, these notes can be converted, at investors’ discretion, into equity in the company so long as the notes are “in the money” (i.e., when the company’s share price exceeds the conversion price, making conversion to equity economically favorable). However, if the maturity date comes and the notes are out of the money, then additional capital is required to cover the liability – this is where concerns about the treasury company playbook stem from. Separately, albeit less frequently discussed, is the risk that these companies may lack sufficient cash on hand to service the interest on their debt. In either event, treasury companies have four main options. They can:

Sell their crypto stashes to shore up cash, possibly hurting asset prices, a move that can affect other treasury companies holding the same asset;

Issue new debt to cover the old liability, effectively refinancing the debt;

Issue new equity to cover the liability, which is similar in nature to how they fund treasury asset purchases through equity financing today; or

Go into default if the value of their crypto stashes doesn’t fully cover the liability.

The path each company takes in the worst-case scenario will depend on specific circumstances and market conditions at the time of maturity; for example, treasury companies can only refinance when market conditions allow.

Then there are equity sales, where the treasury company issues stock to fund asset purchases. The equity sales that are used to supplement asset purchases are less of a concern in the big picture because under this method, there are no obligations for companies to default on, and no liability is created to fund asset purchases.

In our June 4 report surveying the crypto leverage landscape, we examined the magnitude and maturity timeline of the debt issued by some bitcoin treasury companies. Based on what we found, we don’t think there is an imminent threat today as much of the market believes, because most of the debt matures between June 2027 and September 2028. Concern about the debt-driven strategies of treasury companies is not unreasonable given the industry’s history with leverage, but at this time, we do not see significant risk from the approach. This may not always remain the case, however, as the debt comes due and more companies adopt the strategy, possibly taking riskier approaches and issuing debt with tighter maturity timelines. Even in a worst-case scenario, these companies will have a range of traditional finance options to engineer their way out that may not end in the sale of treasury assets.

More recently, we again kicked the tires of the treasury business model in our report entitled “Why are Bitcoin Treasury Companies Trading at Such High Premiums to NAV.” Read it here.

002 Accelerated Demand for Stablecoin

June marked a pivotal moment for the stablecoin sector, driven by two major developments: Circle’s public market debut and the Senate’s passage of the GENIUS Act, the first comprehensive stablecoin legislation in the U.S.

Circle, the second-largest stablecoin issuer globally, became the first stablecoin-native company to go public in U.S. markets. Its shares surged more than 6x during the month. While the magnitude of the move suggests the IPO was initially underpriced, it also reflects strong investor demand and a growing recognition of stablecoins as foundational to financial infrastructure.

Later in the month, regulatory momentum took a significant step forward. On June 25, the U.S. Senate passed the GENIUS Act with a 68–30 vote. The passage marked the culmination of more than a month of procedural votes and political hurdles, including a dramatic cloture vote on May 8 that failed due to a last-minute dispute. It now heads to the House, where some lawmakers have proposed merging it with the broader CLARITY Act. The likelihood of such consolidation is uncertain, especially given President Trump’s public opposition.

Against this backdrop, corporate interest in stablecoins is accelerating. U.S. retailers like Walmart and Target are exploring the option to pilot their own stablecoins, while Mastercard is expanding support by integrating with Paxos’, Fiserv’s, and PayPal’s stablecoins. These companies are not only issuing tokens but also competing to be the first and most widely adopted in terms of circulation and utility. The focus is shifting toward getting stablecoins into real-world payment flows, where scale and user reach will determine long-term success. Internationally, this momentum is echoed by efforts such as Ripple’s regulatory approval for its RLUSD stablecoin in Dubai and Korea’s central bank exploring a won-based stablecoin, though domestic developments remain the most advanced.

Stablecoins are only the entry point. They mark the first stage of bringing traditional fiat currencies onto blockchain infrastructure that is faster, more interoperable, and accessible around the clock. The next phase is focused on bringing financial assets on-chain, starting with tokenized stocks. Robinhood recently introduced tokenized equity trading for 200 publicly listed stocks, now available to European users. This marks an early test of investor demand and execution quality for replicating traditional securities in tokenized formats. Coinbase is also pursuing regulatory approval to do the same in the U.S. These early moves are laying the groundwork for bringing a wider range of traditional financial products on-chain, and we expect private credit and structured funds to be the next assets to be tokenized.

003 12 Days That Shook The World (Markets, Not So Much)

The 12-day conflict between Israel and Iran that began on June 13 barely affected risk assets. At the start of the conflict, crypto prices didn’t react strongly, and equities held steady. However, when the U.S. government intervened and launched Operation Midnight Hammer on June 22, targeting Iranian nuclear facilities, crypto prices dropped sharply. Prices quickly rebounded after Trump announced a ceasefire deal on June 24. Sporadic missile activity continued through the end of the month, and the war has not come to a definitive end.

BTC climbed during this period, moving in step with equities rather than acting as a flight-to-safety asset. This contrasts with what we observed in April and May, when the store-of-value narrative was more prominent amid tariff uncertainties and global bond market stress. BTC’s resilience and outperformance relative to gold and the broader crypto market may be explained in part by strong institutional support, including $4 billion in spot ETF inflows over the month, accelerated purchases from treasury-focused companies, and emerging signs of sovereign buying. This suggests that the war’s impact on BTC was a short-lived macro shock.

Still, the Iran–Israel conflict prompted renewed focus on the crypto infrastructure within Iran, especially its mining sector. Iran has historically played a non-negligible role in Bitcoin mining activities. A 2021 estimate by Elliptic suggested that 4.5% of global Bitcoin mining was conducted in Iran, aided by low-cost, government-subsidized electricity paid in Iranian rial. Given that mining revenues are denominated in BTC, this structure creates a favorable profit margin for local operators, particularly during BTC bull cycles.

Following the Israeli and American strikes, rumors circulated that some of Iran’s mining infrastructure may have been damaged, contributing to a perceived drop in network hashrate. However, short-term hashrate fluctuations often reflect noise or block timing variance rather than systemic impairment. Without longer-term moving averages or granular regional data, there’s no verifiable evidence yet of meaningful mining disruption stemming from the conflict. There are also other proposed explanations for the drop, including the heatwave in the Northeast and Midwest, which prompted Bitcoin miners in those regions to scale back their operations.

Beyond infrastructure, the war also reignited discussion of crypto’s role in the Iranian financial system. Due to decades of high inflation, international sanctions, and a chronically unstable peg to the U.S. dollar, crypto adoption in Iran has deepened across civilian and informal economic channels. Historical data from Chainalysis suggests that during previous conflict periods, including missile exchanges and the 2024 assassination of a Hezbollah leader, crypto outflows from Iran tended to increase.

Bitcoin and Tron have historically been the primary networks used in Iran, particularly with Tron facilitating USDT transfers. However, during this conflict episode, there was no visible surge in stablecoin transactions or on-chain settlement volumes that would indicate a material change in crypto usage patterns on either network. On-chain activity among short-term holders also declined during the period.

While there was no major shift in on-chain activity, the crypto industry did surface in the conflict through a symbolic episode: the $90 million hack of Nobitex, Iran’s largest crypto exchange. The attacker, a pro-Israeli group named “Predatory Sparrow,” was reportedly able to steal funds and send them to brute-force wallet addresses containing provocative anti-IRGC messages such as “F*ckiRGCTerrorists.” Nobitex has previously been linked to financial flows involving IRGC-affiliated entities, and the attack appears to have been a form of cyber-psychological warfare rather than a financially motivated operation.

Iran is an example of the country where currency devaluation is severe and is globally sanctioned. For these societies, crypto does function as an important funnel for money movements. The visibility of crypto in the political and cyber dimensions of the conflict show that crypto has now also become an important part of the financial system.

004 Our Takeaways and Predictions

Heading into July, markets will be closely monitoring several key developments that could influence macro conditions and asset prices. The expiration of the current tariff pause is scheduled for July 9, though some progress appears to be underway. Treasury Secretary Bessent stated that he expects trade negotiations to conclude by Labor Day, with one agreement already secured with Vietnam and others reportedly in progress. On the domestic front, the “One Big Beautiful Bill Act” was signed into law by President Trump on July 4. The bill could significantly widen the federal deficit, which is already running above expectations, based on the latest economic data.

Inflation remains a key consideration, but recent data suggests pressures are easing. The core personal consumption expenditures (PCE) index has been trending lower, with only one monthly increase in February, likely driven by front-loaded pricing effects tied to the tariff timeline. While inflation appears contained for now, the real risk lies in the Fed cutting rates too early, which could re-accelerate inflation.

The labor market remains tight, giving the Fed more flexibility in decision-making. June payrolls came in better than expected, and the unemployment rate fell to 4.1%, lower than the most optimistic forecast. This drop is partly explained by a shrinking labor force, with participation falling from 62.4% to 62.3%. As of now, market-implied odds for a July rate cut have fallen to zero, with approximately two cuts priced in by year-end depending on how tariffs and growth data evolve.

A final trend to watch is the continued weakness of the U.S. dollar. Economic uncertainty, unresolved fiscal policy, and the prospect of rate cuts later this year have all contributed to downward pressure on the greenback. The U.S. Dollar Index is now on track for its worst January-to-June performance since 1973. Risk assets are priced in dollars, so a weaker dollar helps explain the resilience in equities and the strength in BTC despite mixed fundamentals. With the M2 money supply nearing all-time highs and markets awash in liquidity, the dollar could remain under pressure, especially if the Fed pivots toward easing in the second half of the year.

Key Events to Watch:

July 8: Expiration of Tariff Pause

July 30: FOMC

Key Macroeconomic Data Releases:

July 11: CPI

July 16: PPI, US Beige Book

To learn more about the topics covered in this month's newsletter, contact our team or reach out to your Galaxy representative.

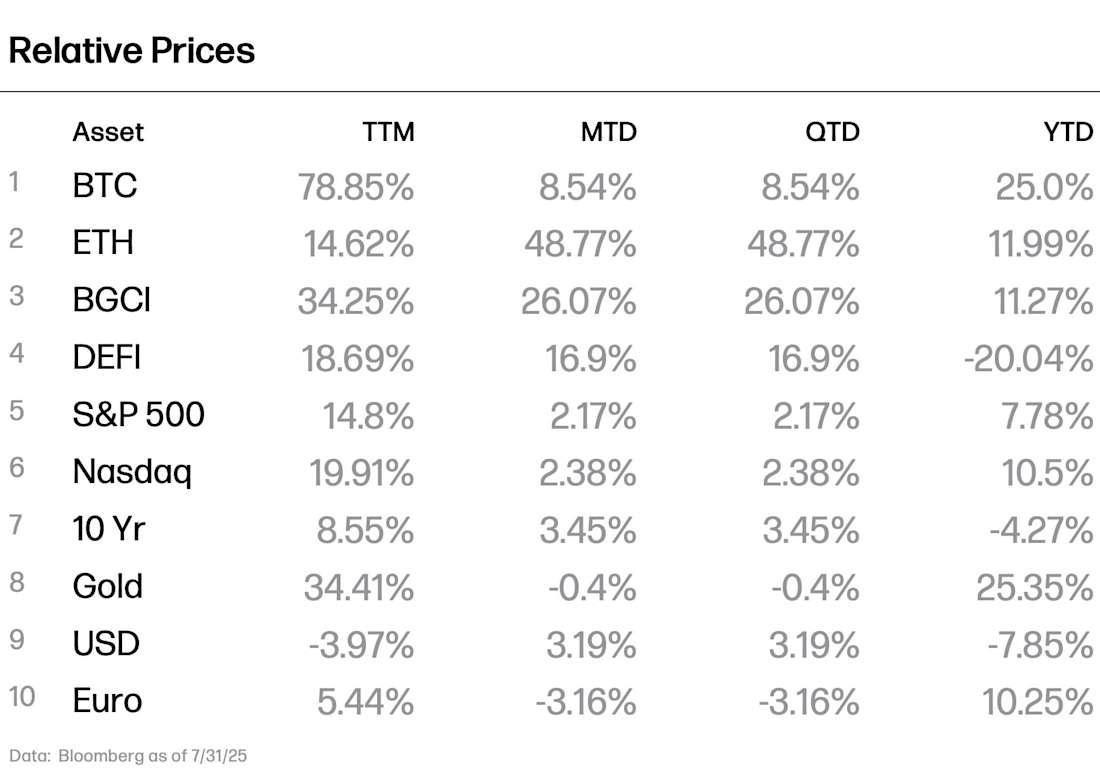

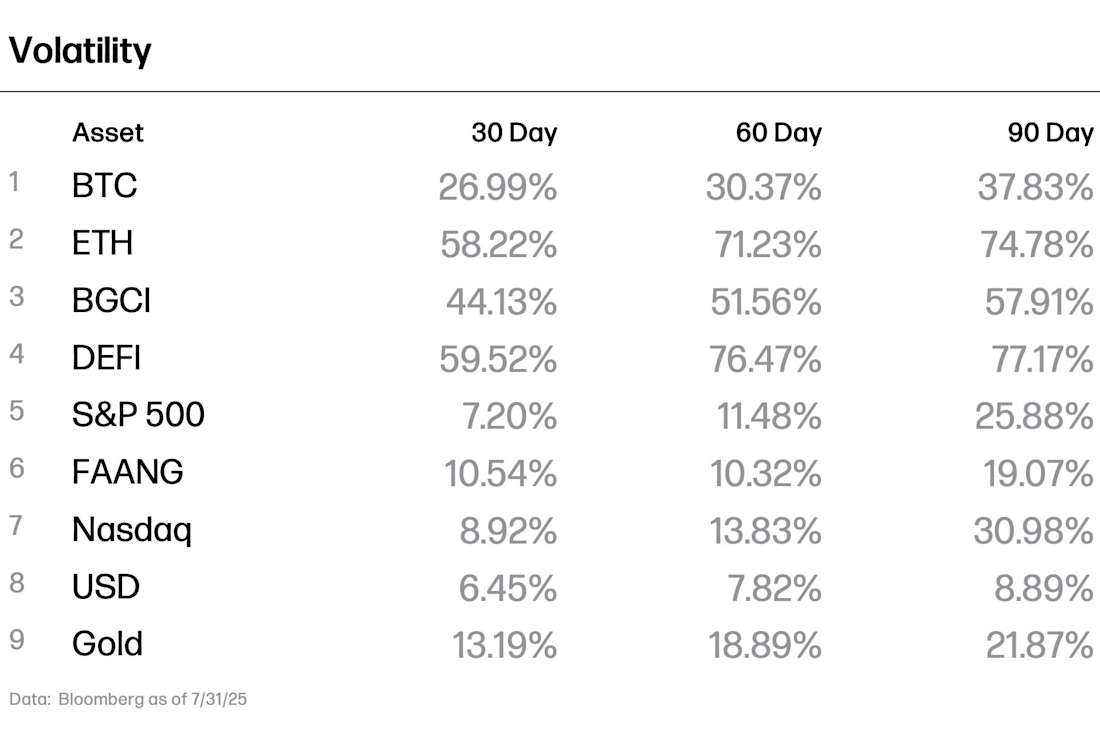

Crypto Performance & Volatility Data