The October Edition

By Jianing Wu

September was defined by broad strength across risk assets as expectations for Federal Reserve easing firmed. Weaker labor data early in the month reinforced the case for multiple cuts by year-end, helping propel U.S. equities to fresh all-time highs. Technology and AI-driven names led performance, while gold surged to record levels as investors sought protection from uncertainty and exposure to assets poised to benefit from easier monetary policy. The combination of disinflation signals and rate-cut momentum set a supportive backdrop across various asset classes, lifting equities and crypto on expectations of easier policy, while driving demand for gold and other real assets as yields declined.

Crypto markets reflected that same mix of optimism and volatility. In early September, spot BTC ETFs logged their strongest inflows in weeks, reversing the August pattern of ETH leadership and underscoring BTC’s role as digital gold alongside bullion’s rally. ETH outperformed BTC mid-month on the back of strong corporate treasury allocations and rising onchain activity. Stablecoin supply also climbed steadily toward $300 billion, with DeFi-native issuers driving ecosystem integrations while TradFi firms advanced payment-focused initiatives.

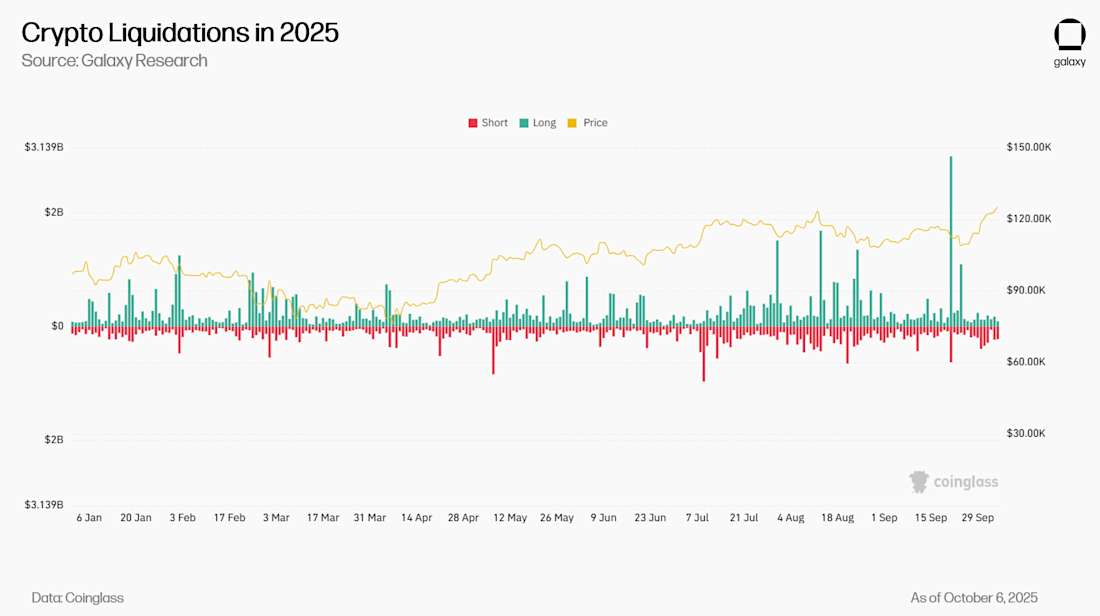

However, crypto endured its sharpest liquidation event since early 2021 in the last week of September. A wave of forced unwinds in BTC and ETH derivatives briefly pushed BTC below $110,000, ETH below $4,000 and drained leverage across the market. The selloff was short-lived, however, as ETF flows and institutional accumulation stabilized sentiment and reset positioning.

That momentum has carried into early October. BTC has reclaimed $120,000 and hit a new all-time high, ETH is back above $4,600, U.S. equities are trading at record highs, and gold continues to climb to new peaks. The synchronized rally across crypto, equities, and commodities suggests renewed investor conviction and suggests that September’s volatility ultimately reset markets for another leg higher.

Crypto ETFs Hit the Fast Track: In September, U.S. regulators fast-tracked crypto ETF approvals, setting the stage for a new wave of institutional crypto products.

Solana Szn: Solana enters the ETF era with powerful tailwinds. Record network activity, rising institutional accumulation, and a major performance upgrade position it as a leading high-throughput blockchain in crypto.

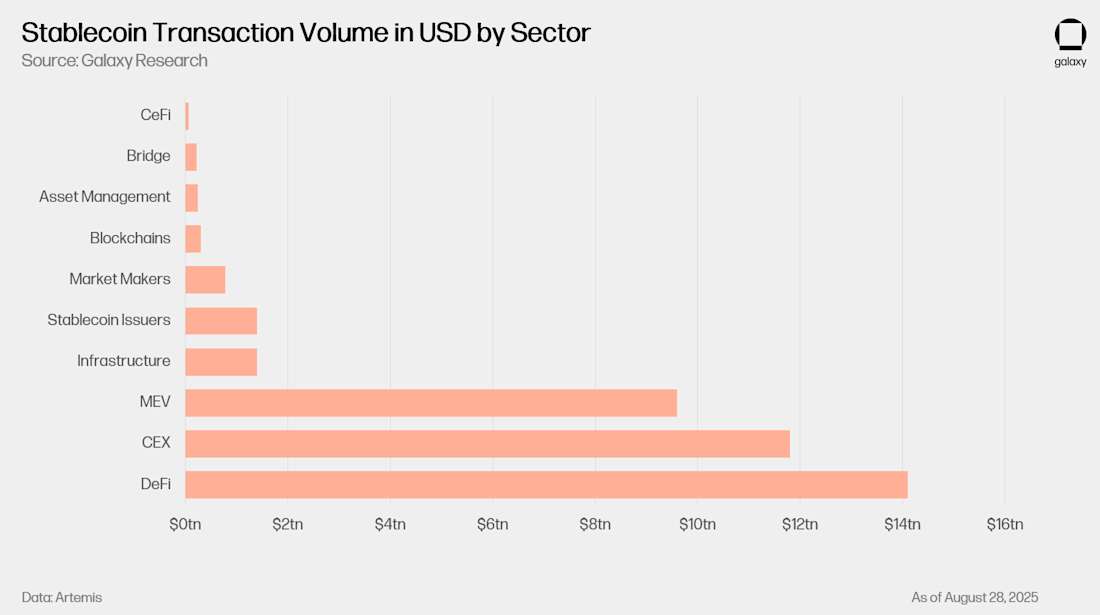

Stablecoins – Converging on One Big Market: Stablecoins have become one of the fastest-growing segments in digital assets, surpassing $300 billion in supply as crypto-native issuers deepen integration in DeFi and TradFi giants race to capture global payments and settlement markets.

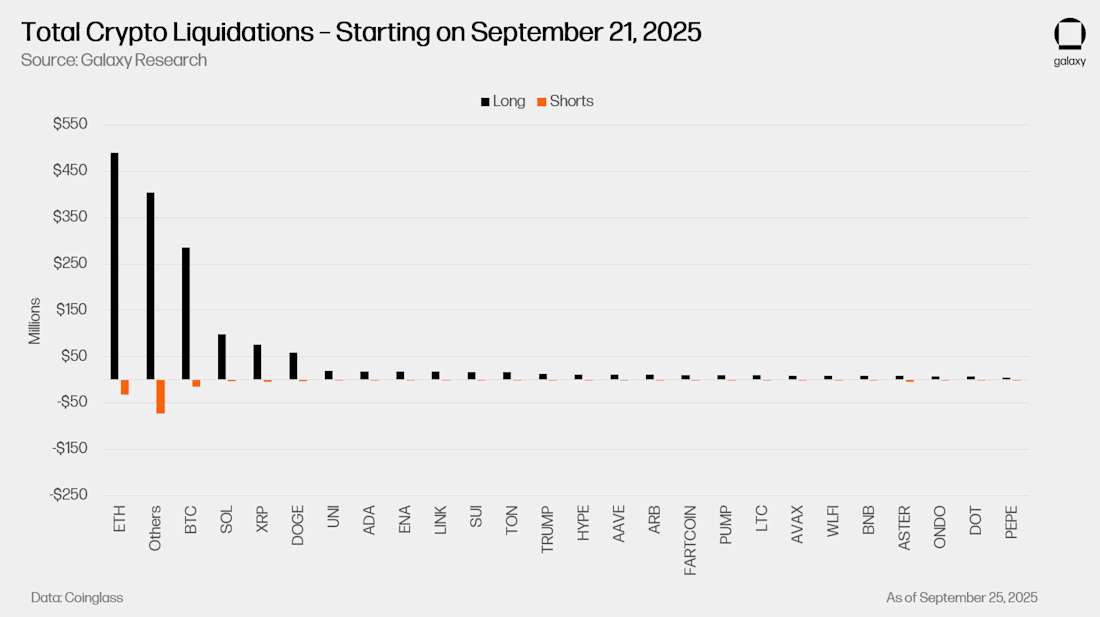

The Great September Shakeout: A $1.7 billion wave of liquidations on September 21 triggered crypto’s sharpest reset in years, flushing out leveraged longs but revealing renewed accumulation as large investors took advantage of the price drop.

001 Crypto ETFs Hit the Fast Track

It was a big month for crypto exchange-traded funds in the U.S.

On September 2, the Securities and Exchange Commission (SEC) and Commodity Futures Trading Commission (CFTC) issued a joint statement allowing registered exchanges to list spot crypto products with leverage and margin, bringing these markets under joint oversight which could improve transparency and liquidity. On Sept. 30, the SEC issued a no-action letter confirming that state-chartered trust companies can act as qualified custodians for crypto assets. The move broadens the field of providers, intensifies competition, and sets custody on a path toward commoditization. Meanwhile, global banks Citi and State Street plan to enter the crypto custody market in 2026, with other major banks expected to follow.

The biggest story, arguably, came on September 17, when the SEC approved new fast-track standards for crypto ETF listings. The rule shortens the approval timeline from as long as 270 days to 75 days or less. The key requirement is the existence of a regulated futures market for the underlying asset with at least six months of trading history. According to our internal analysis, besides BTC and ETH (which are already in ETFs), 10 assets fit the bill: DOGE, BCH, LTC, LINK, XLM, AVAX, SHIB, DOT, SOL, and HBAR, with ADA and XRP to soon follow. Prospective issuers of ETFs tied to these coins were asked to withdraw their 19b-4 filings, because they are now automatically covered under the new generic listing standards. With the framework in place, the pipeline for altcoin ETFs should accelerate and we expect more spot crypto products to be launched in the coming months.

Two days later, on September 19, Grayscale launched the Coindesk Crypto 5 ETF (GDLC), the first multi-asset exchange-traded product (ETP) in the U.S., offering exposure to BTC, ETH, XRP, SOL, and ADA. This product signals the beginning of index-style offerings, a natural next step in market development.

Next, we expect to see at least one U.S. spot Solana ETF with staking: Galaxy’s own. We initially expected a launch this week, but the government shutdown will likely delay the necessary approvals. In Canada, Solana spot ETFs have been trading since April 16 and have accumulated $319 million in inflows, equivalent to about 0.2% of SOL’s market cap. This is modest compared with BTC, where U.S. spot ETFs attracted net flows equal to 0.8% of BTC’s market cap within their first three months, but it reflects steady adoption in a smaller Canadian capital market.

Other altcoin ETFs launched in September, though without providing pure spot crypto exposure. Dogecoin and XRP ETFs came to market with varying degrees of direct exposure, often retaining the flexibility to hold futures instead of spot assets. For these products, inflows are likely to be more modest. There may be investor demand for such vehicles, but they are unlikely to approach the scale of BTC, ETH, or even SOL, given differences in adoption, utility, and perceived risk of the underlying coins.

We think that in general, altcoin ETF inflows will depend heavily on market sentiment and rotation dynamics in crypto. BTC dominance fell from 60% at the start of August to 54.8% at the end of September, while ETH’s share of total crypto market cap edged up from 11.7% to 12.0%. These numbers suggest that it’s still altcoin season. A supportive, risk-on macro backdrop will also be critical in sustaining flows into higher-beta altcoins. Over time, while broad-based crypto ETFs will appeal to some investors, flows are likely to concentrate in coins with proven network utility and established track records, leaving riskier tokens with smaller allocations.

002 Solana Szn

With a spot Solana ETF expected to launch soon if not imminently, investor focus is shifting toward the network’s fundamentals and long-term drivers. Beyond near-term market flows, Solana’s ecosystem continues to demonstrate scale and resilience.

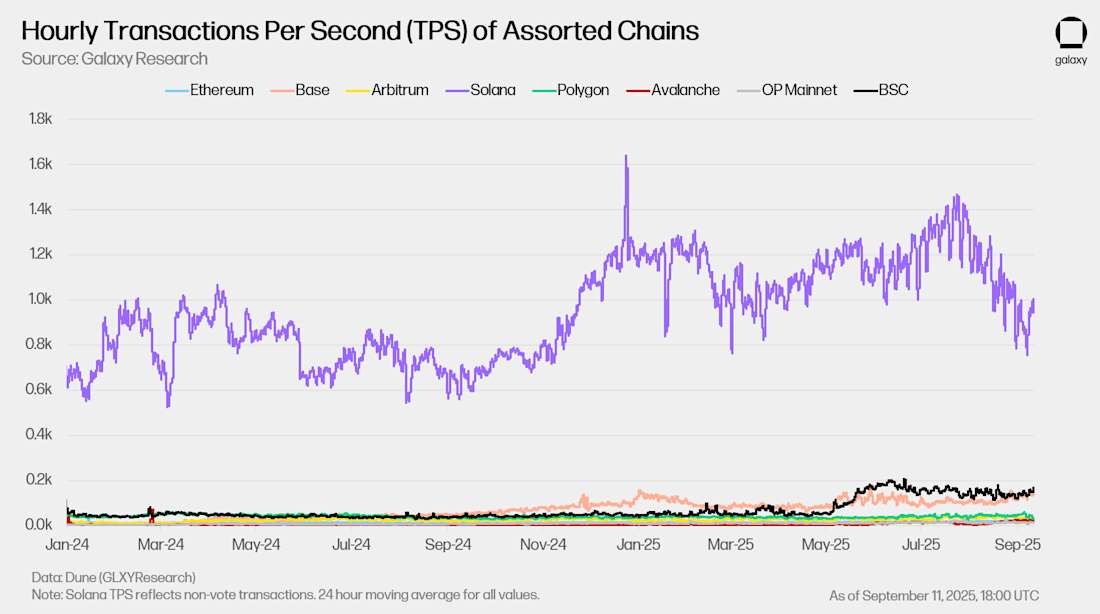

Solana has consistently ranked at the top of major blockchains in terms of block space demand and application-level value creation. Over the past two years, it has maintained the highest throughput among leading chains, processing activity at multiples of competitors such as Ethereum’s L2 Base, Binance Smart Chain, and Arbitrum. Even in periods of slower usage, Solana processes several times more transactions per second than other networks, a sign of capacity and sustained demand for its block space.

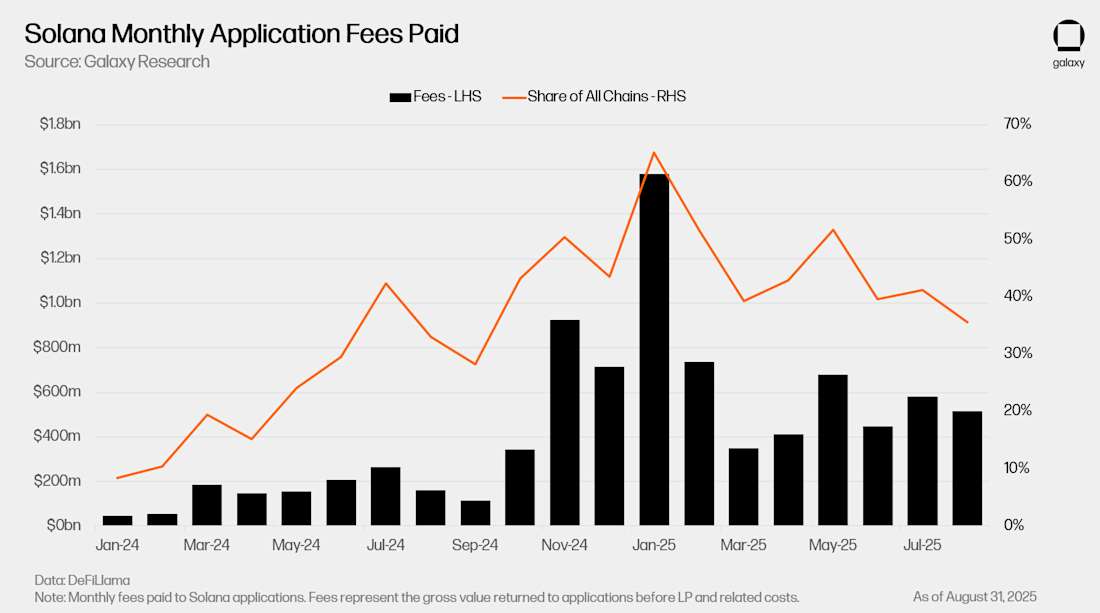

That demand translates directly into economic activity. For nearly a year, Solana has led all blockchains in fees paid to applications, a measure of the gross value users pay for things like swaps or borrowing on DeFi protocols. On average, Solana has captured close to half of all application-level fees across blockchains in 2025, underscoring its ability to generate and retain real economic value at scale.

Another emerging tailwind is accumulation by digital asset treasury companies (DATCOs). Holdings of SOL by such companies climbed from 4.5 million SOL in August to 13.6 million in September, with Forward Industries, a Galaxy-backed Solana treasury company, accounting for the majority of new purchases (~6.8 million). Other firms, such as DeFi Development Corp, have also been accumulating, albeit at a smaller scale. This balance sheet allocation suggests growing institutional confidence in Solana’s role as a core network asset and may become a structural source of demand alongside ETF flows.

Looking ahead, Solana’s next major upgrade, Alpenglow, proposed in May and slated for a public testnet launch in late 2025, is designed to push performance and efficiency even further. The upgrade is expected to improve user experience, strengthen network resilience, and make Solana more attractive for builders. In effect, Alpenglow positions Solana to compete not only with other blockchains, but also with the speed and reliability standards of traditional finance infrastructure.

With strong application demand, growing treasury accumulation, dominant transaction throughput, and a major upgrade on the horizon, Solana enters the ETF era with structural tailwinds.

003 Stablecoins: Converging on One Big Market

Stablecoins remain one of the fastest-growing corners of digital assets, with total supply breaking $300 billion in early October. Growth is being driven from two directions: crypto-native issuers building deeply into DeFi ecosystems and TradFi players targeting payments and settlement rails. Both efforts are accelerating and the competition for market share is intensifying.

On the crypto side, stablecoins are already central to the DeFi economy, powering decentralized exchanges, lending protocols, and yield farming. The integration is so deep that capturing a stablecoin ticker or role in a DeFi ecosystem can represent billions in value, especially on a leading decentralized exchange like Hyperliquid.

An event closely watched by the crypto community, Hyperliquid held its first major governance vote on which issuer would claim the coveted USDH ticker (read Galaxy Research’s analysis here). With billions in USDC flowing through the network and hundreds of millions in annual yield captured externally by Circle, securing the ticker represented a chance for Hyperliquid to internalize that value. The bid was eventually won by Native Markets, a Hyperliquid-aligned infrastructure provider.

At the same time, the largest stablecoin issuers are repositioning themselves for U.S. regulation. On September 12, Tether announced plans to launch of USAT, a stablecoin designed to comply with the U.S. GENIUS Act. Anchorage Digital Bank would formally issue the coin, Cantor Fitzgerald would custody the reserves, and Bo Hines, former Executive Director of the President’s Working Group on Digital Assets, would serves as CEO of Tether’s new U.S entity. Rather than retrofitting its $170+ billion offshore USDT product to fit strict collateral requirements, Tether is pursuing a dual-track model: keep USDT highly profitable offshore while creating a compliant product tailored for U.S. markets. This approach protects its core margins while giving Tether optionality if GENIUS-compliant stablecoins become the standard.

TradFi institutions are also circling the opportunity. Internet infrastructure provider Cloudflare introduced the NET Dollar, a stablecoin designed to support AI-driven business models, while SWIFT announced it is adding a blockchain-based ledger to its global interbank messaging network to improve efficiency and real-time settlement.

The takeaway is simple: many entities are entering the stablecoin race because the market is too large to ignore. DeFi-native issuers are competing for deep integration in crypto ecosystems, while TradFi players are building for global payments and settlement. Both channels reinforce the same trends: accelerating adoption and growing competition in a market that now exceeds $300 billion in supply and could be the first crypto sector to reach a trillion-dollar scale.

004 The Great September Shakeout

For more detail on this stories, read our original coverage of this story by Christopher Rosa. Subscribe here to receive future updates.

September 21 brought a sharp deleveraging across crypto, with liquidations spiking to highs not seen in four years. More than 400,000 traders were forced out of their positions, and notional liquidations came in just under $1.7 billion. Leverage was extreme, with liquidation maps showing the heaviest clustering in the 50x to 100x buckets, leaving prices especially vulnerable to a cascade. The washout underscores how dependent recent price action has been on leverage and thin weekend liquidity.

Liquidations are forced closures of a margined or collateralized position when losses or collateral shortfalls push an account below its maintenance margin. ETH led the washout, suffering roughly twice the notional liquidations seen in BTC. Longs incurred most of the damage while short liquidations were modest. Traders who had built aggressive long positions in anticipation of continued upside quickly found themselves on the losing side as cascading liquidations amplified the decline.

However, onchain signals suggest accumulation rather than panic. Over 420,000 ETH were withdrawn from exchanges during the following week, and at least 15 wallets acquired more than 406,000 ETH (worth over $1.6 billion) later that week, signaling that whales have been seizing the buy opportunities. Despite the volatility, momentum around forthcoming ETF launches has kept sentiment cautiously optimistic, and crypto markets have regained momentum in early October.

005 Our Takeaways and Predictions

We remain optimistic heading into October. The month has opened with strong momentum as BTC surged above $123,000 and ETH moved back above $4,500, even against the backdrop of a government shutdown. Macro conditions remain supportive, with the Fed cutting rates in a resilient economy, equities at record highs, and gold extending its rally.

The structural drivers for crypto adoption are also strengthening. Regulatory clarity around the crypto products is improving, with additional ETF launches expected in the coming weeks. Distribution is widening as major platforms move to integrate crypto exposure, with Morgan Stanley’s E*Trade planning to allow clients to trade cryptocurrencies and Vanguard preparing to permit crypto ETF trading, a critical step in mainstream integration.

On the macro side, the prospect of further tariffs raises the risk of a weaker dollar, which historically has supported flows into BTC as a hedge. Combined with regulatory progress and broadening institutional access, the setup for an Uptober is favorable.

Key Events to Watch:

October 13: CME options launch for SOL and XRP

October 29: FOMC Rate Decision, Powell Speech

Key Macroeconomic Data Releases:

October 10: University of Michigan Preliminary Consumer Sentiment & Preliminary Inflation Expectations

October 15: Consumer Price Index

October 16: Producer Price Index

October 30: Advance GDP Quarter-over-Quarter

October 31: Core Personal Consumption Expenditures Price Index

To learn more about the topics covered in this month's newsletter, contact our team or reach out to your Galaxy representative.

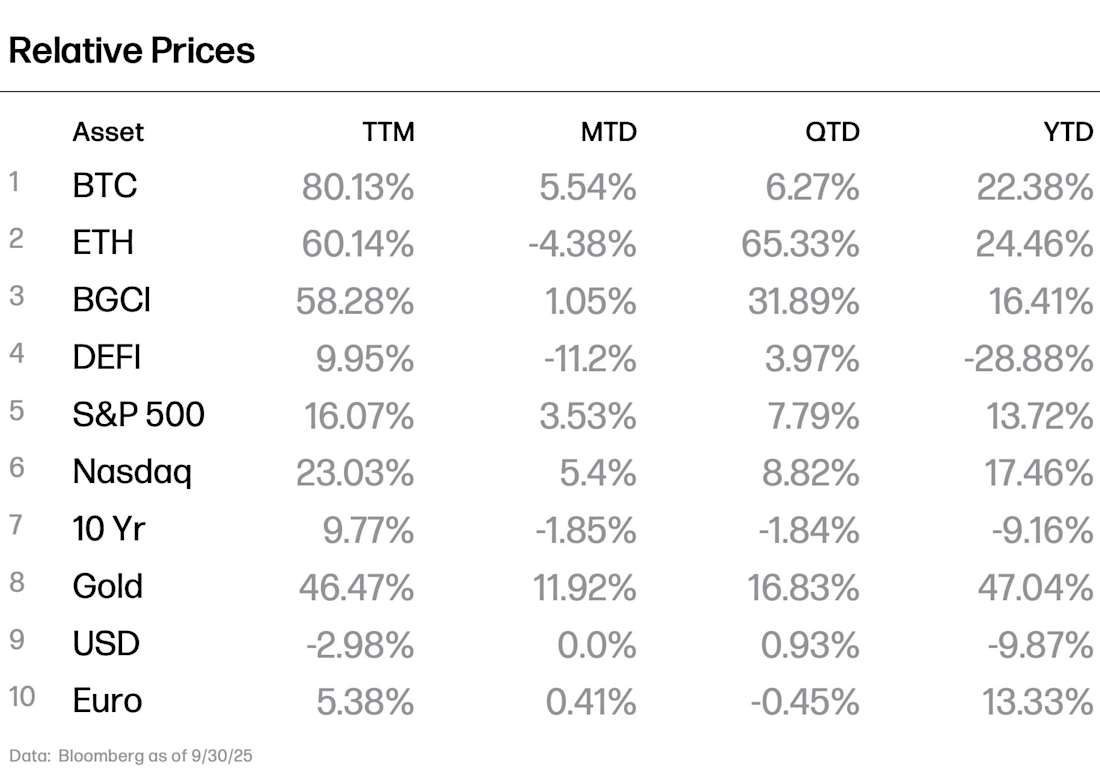

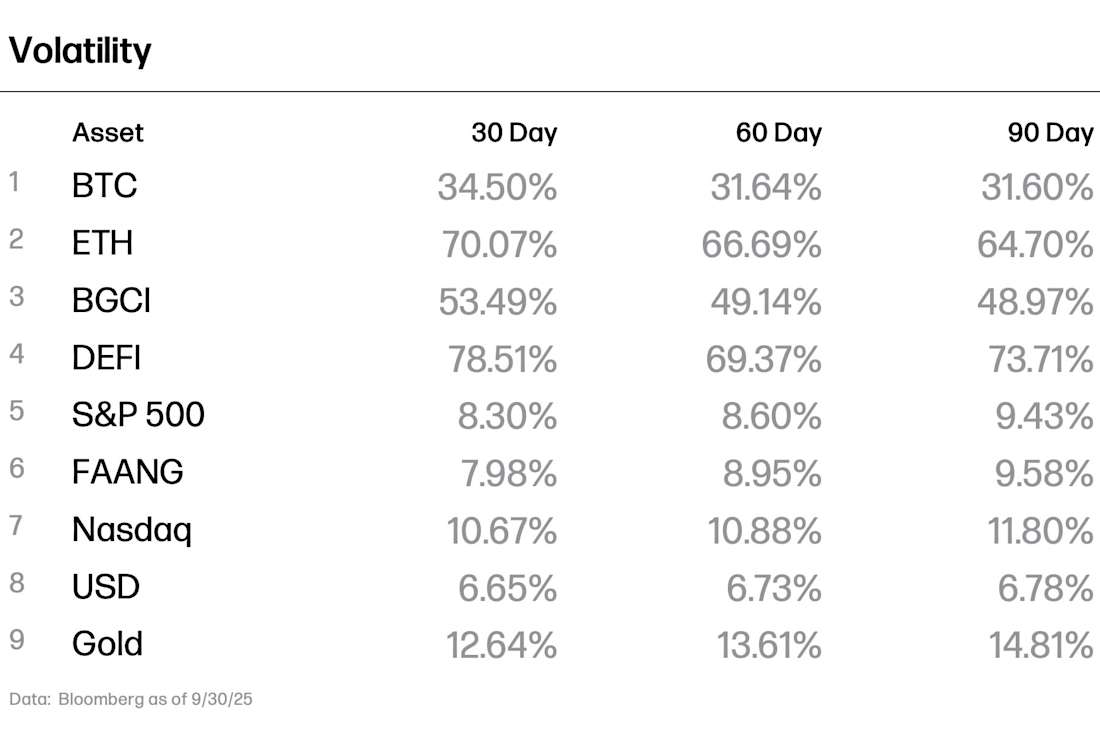

Crypto Performance & Volatility Data