The June Edition

By Jianing Wu & Su Young Lee

Crypto markets posted strong performance through most of May, fueled by a combination of macro drivers and growing institutional demand. BTC surged to an all-time high around $112k mid-month, extending its run as a store of value amid global fiscal uncertainty. ETH gained more than 40% over the month, rebounding from recent lows and reclaiming ground versus BTC as the ETH/BTC ratio rose from 0.018 to 0.024.

The macro environment was mixed but generally supportive. Early in the month, equities rallied on softer inflation prints and easing trade tensions, highlighted by a temporary U.S.–China tariff détente and a U.S.–UK deal. Later, fiscal worries reemerged after Moody’s downgraded the U.S. credit rating and lawmakers advanced a large tax-cut and spending bill, pushing yields higher and pressuring risk assets. Despite some week-to-week volatility, crypto remained resilient, with BTC outperforming tech equities and ETFs showing strong flows, until a modest pullback during the final week of May as trade policy fears resurfaced.

All of this set the stage for a show of force at Bitcoin 2025 in Las Vegas, where more than 30,000 attendees gathered to celebrate Bitcoin’s growing relevance. From Vice President J.D. Vance promising policy support to Jack Dorsey’s Block rolling out Lightning payments at checkout, the tone was unabashedly bullish. The event captured the institutional shift now underway: crypto is no longer a fringe asset class; it’s being adopted across balance sheets, embedded in infrastructure, and discussed at the highest levels of government. That growing engagement is the focus of this month’s commentary.

BTC Hits ATH: BTC surged to $112k amid fiscal stress and rising global demand for non-sovereign assets.

ETH Rebounds: ETH rallied 35% as the Pectra upgrade and L1 narrative regained investor attention.

Stablecoin Legislation Advances: The GENIUS Act cleared Senate cloture, signaling real progress on dollar-backed digital asset regulation.

Institutional Adoption Accelerates: From ETFs to treasuries to tokenization, institutional adoption deepened across capital, infrastructure, and on-chain deployment.

001 BTC Hits ATH

BTC reached a new all-time high (ATH) of $112,000 on May 22, following a week of decisive upward momentum. It broke through prior highs throughout the week – starting with Wednesday’s $109k, ripping past $110k, and touching $112k. The previous all-time high was set on January 21, the day after Trump’s inauguration, at approximately $107k. From there, over the past four months, BTC suffered a sharp correction to $77k, a ~39% decline driven by tariff uncertainty, geopolitical instability, and a weakening macroeconomic outlook. By May 31, BTC had retreated along with global assets to the $103k - $105k range.

BTC’s breakout is supported by signals across derivatives markets. Open interest across all exchanges hit an ATH, and the call-put ratio on major exchanges held steady at 1.5. Meanwhile, short-term implied volatility dropped to an 18-month low of 35 - 40%. This mix of bullish sentiment and compressed volatility typically suggests excess leverage is building, and it likely served as a key driver in pushing BTC through resistance.

We find the timing of BTC’s ATH remarkable. This rally defied broader market weakness as U.S. equities (S&P 500 and Nasdaq 100) dropped and Treasury yields rose. Gold’s 0% return this month was dwarfed by BTC’s 10.8%. BTC is increasingly behaving like a store of value as it moves in tandem with gold but outperforms the precious metal in both magnitude and momentum as the cryptocurrency enters a new phase of price discovery.

The rally in BTC may have been sparked by Moody’s downgrade of the U.S. credit rating from Aaa to Aa1. The rating agency cited unsustainable fiscal dynamics and a ballooning $36 trillion debt load. Following the downgrade, equities, bonds, and the USD declined, while BTC and gold rose, an early signal that markets were repricing risk and warming to non-sovereign assets.

The repricing continued throughout mid-May. Long-end U.S. Treasury yields rose significantly, with the 30-year yield reaching 5.14% on May 22, its highest level since 2007. This was preceded by a weak 20-year auction on May 21, where investor participation faltered amid mounting concerns over fiscal deficits and growing debt.

Importantly, this dynamic is not isolated to the U.S. In Japan, yields on 30- and 40-year government bonds also hit ATHs on May 22 following a poorly received auction, which drew the weakest demand since 2012. The Bank of Japan’s reduction in bond purchases, coupled with a Q1 economic contraction, is weighing on Japan’s debt market. Long-end yields in the U.K., Canada, and Europe have also climbed, reflecting global investor unease around inflation, trade war, fiscal policy, and sovereign creditworthiness.

These developments have cast a harsh light on debt sustainability on a global scale. In the U.S., that backdrop became even more complex when lawmakers advanced a substantial multi-trillion-dollar tax and spending package pushed by the Trump administration. The House Budget Committee approved a proposal incorporating state and local tax (SALT) deductions and expansive tax cuts, which could add $5.2 trillion to the national debt and increase the federal deficit by $600 billion next fiscal year. This comes at a time when investor tolerance for deficit expansion is already showing signs of fatigue.

Against this backdrop, BTC and gold are emerging as preferred hedges. With traditional safe-haven assets under pressure, BTC’s non-sovereign, supply-constrained nature is gaining increased relevance.

Institutional and sovereign adoption continues to provide consistent price support. On May 19, Strategy (formerly MicroStrategy) purchased 7,390 BTC, while Metaplanet acquired 1,004 BTC, its second-largest purchase to date. Strategy further filed on May 22 to raise up to $2.1 billion through a 10.00% Series A perpetual preferred share issuance (STRF) to fund additional BTC purchases. These actions reinforce a steady stream of corporate demand.

On the access front, JPMorgan’s CEO told CNBC it will offer BTC trading to clients (notwithstanding his longstanding reservations about the asset), joining a wave of traditional financial institutions expanding into crypto. Other major banks – including Morgan Stanley, Merrill Lynch, and Wells Fargo – are either enabling or preparing to support crypto and crypto ETF trading.

All told, BTC is increasingly trading in line with its foundational value proposition: a scarce, decentralized, and non-sovereign store of value. As it enters price discovery in a different macro environment, these attributes are becoming more salient.

002 ETH Is So Back

Following months of poor performance, ETH finally got its pump. After hitting a five-year low of 0.018051 on April 21, the ETH/BTC ratio staged a sharp rebound, climbing 34% to reach 0.024170 on May 31. The bulk of this move occurred between May 7 and May 10, when the ratio surged from 0.018666 to 0.024659. Over the same period, ETH's price jumped from $1,812 to $2,583. ETH has since stabilized around $2,600, broadly in line with the overall market.

The rebound was accompanied by a modest 0.76 percentage point rise in BTC dominance, to 62.94%, and a slight uptick in ETH’s share of the overall crypto market cap by 2.32 points between May 7 and May 31, to 9.42%. Additionally, ETH’s open interest leverage ratio hit an all-time high, indicating an elevated risk appetite and a market skewed toward bullish positioning with a decreasing put/call ratio.

While a 35% price increase looks impressive, the move was concentrated within a three-day window from May 7 to May 10. During that time, the total crypto market cap jumped from $3.096 trillion to $3.494 trillion, a 12% increase. Altcoins also rallied broadly alongside ETH; memecoins saw a 43% rise in market cap, while DeFi tokens climbed 29.5%. Since May 10, ETH has largely traded in line with the broader market, fluctuating around the $2,600 level.

The rally coincided with the implementation of Ethereum’s Pectra upgrade. While Pectra certainly deserves attention, the more meaningful takeaway may be the narrative it reinforces: Ethereum’s renewed focus on improving the L1 experience. Pectra was designed to enhance user and validator experiences directly on L1.

For instance, among the 11 Ethereum Improvement Proposals (EIPs) included in Pectra, EIP-7702 introduces a significant improvement by adding smart contract capability to externally owned accounts (EOAs). This change could improve wallet design and address longstanding criticisms of Ethereum’s user experience. Another major upgrade is EIP-7251, which raises the validator staking limit from 32 ETH to 2,048 ETH. This encourages validator consolidation, reduces coordination overhead, and improves scalability on the Ethereum mainnet.

The Pectra upgrade also comes after a shakeup of the Ethereum Foundation leadership, which now operates under a dual Executive Director structure to enhance responsiveness and transparency. One of the focuses iterated by the foundation is on pursuing the “success of the Ethereum mainnet protocol” (while “supporting the success of L2 chains”) by “improving the developer and user experience, clarifying standards, strengthening ecosystems, and smoothing the journey from ideas to live applications.” Meanwhile, Ethereum creator Vitalik Buterin has proposed replacing the Ethereum Virtual Machine (EVM), the computation engine at the heart of the network, with RISC-V, again with the goal of improving mainnet performance, modularity, and compatibility.

It's too early to say whether these upgrades will have a tangible impact on L1 usage. Adoption of EIP-7702, for example, remains limited, with only 74,000 EOAs upgraded so far, compared to roughly 500,000 daily active mainnet addresses. In this light, Pectra’s significance may lie less in immediate utility and more in what it signals: a clear attempt to shift the narrative back toward restoring the L1.

Alongside ETH’s price surge, we've also seen a reversal in U.S. spot ETH ETF flows, which had been negative from early February through mid-April. The reversal suggests renewed institutional optimism, perhaps driven by growing interest in tokenization and stablecoin development, topics that have recently gained traction in the headlines.

However, while Ethereum has so far captured the lion’s share of tokenization activity, its dominance has been concentrated in areas like real-world assets (RWAs), including stablecoins. Solana, by contrast, is carving out a niche in tokenized equities and high-velocity asset trading. Its high-throughput, low-cost infrastructure suits it well for these use cases. Recent developments underscore this positioning: the Kraken exchange announced a partnership with Solana to bring tokenized U.S. stocks to non-U.S. clients, and R3 (a survivor from the long-ago heyday of permissioned enterprise blockchains) plans to bring regulated assets onto a chain often associated with memecoins. While it may not directly threaten Ethereum’s lead in broader tokenization efforts, Solana’s differentiated approach could position the chain as a strong complementary player in tokenized public equities and fast-settling digital assets.

In short, ETH’s outperformance in early May was driven by a combination of a risk-on market environment and a narrative pivot back to L1. The question remains whether this L1 narrative can take hold in a sustainable way. With a majority of activity having migrated to L2s, value accrual to ETH on mainnet remains a central challenge.

003 Stablecoin Legislation Advances

The Senate passed the GENIUS Act in March while the House approved its own version, the STABLE Act, in April, raising hopes for bipartisan alignment on stablecoin legislation. However, several Senate Democrats who initially supported the GENIUS Act reversed their votes in early May, citing concerns over anti-money laundering enforcement, the role of foreign issuers, national security risks, and the integrity of the financial system. There is also growing debate around how the law will hold issuers accountable if they fail to meet regulatory requirements.

After intense backroom negotiations including concessions such as a ban on stablecoin issuance by big tech firms, the Senate successfully voted to invoke cloture on May 19, effectively overcoming the previous filibuster and setting the stage for full Senate debate. The change in sentiment was notable: 16 Democrats flipped to support cloture, with key lawmakers such as Senators Alsobrooks (D-MD) and Gillibrand (D-NY) switching their votes from Nay to Yea.

While final passage still requires additional steps, the May breakthrough marked significant legislative progress. The GENIUS Act would impose rigorous standards around collateral management, AML/KYC, bankruptcy-remoteness, customer protection, oversight and supervision, and foreign issuers marketing in the U.S., all of which are critical elements for institutions seeking regulatory clarity on digital dollar infrastructure.

Importantly, we believe this is not a “crypto bill” but rather a dollar infrastructure bill that aims to modernize U.S. monetary instruments for blockchain-based settlement. It creates a compliance framework that invites participation from both crypto-native firms and traditional finance players.

If signed into law, the GENIUS Act could unlock institutional demand for tokenized dollars and new global demand for U.S. Treasuries, while giving regulators the tools they need to oversee a fast-growing, systemically relevant digital asset. The bill’s success or failure will offer a critical signal about Washington’s capacity to lead in shaping the future of digital finance and the U.S. dollar’s ability to remain the world’s reserve asset in the blockchain era.

004 Institutional Adoption Accelerates

With regulatory clarity progressing, institutional participation continues to build. May offered signs of broader institutional momentum across multiple fronts: opportunistic capital allocation, infrastructure adoption, and integration with public blockchains.

Capital Allocation:

Record ETF Inflows: S-listed crypto ETFs saw net inflows of $6.2B in May, marking the strongest month in 2025 and the second-highest monthly inflow on record. Ethereum funds also recorded $402M in net allocations, the third-largest monthly inflow since launch.

CME Derivatives Activities Pick Up: CME SOL futures averaged 900 daily contracts in May, up from 700 in April, while open interest nearly doubled. XRP futures, introduced on May 18 as the newest addition to CME’s crypto assets series, saw $12M notional traded on day one, underscoring sustained demand for regulated access to crypto exposure, regardless of ongoing delays around spot ETF product approvals.

Private Market Activity Accelerates: Crypto-native venture funds such as Theta Capital and Galaxy’s own Venture fund successfully closed new rounds, highlighting renewed institutional interest in early-stage investments.

Treasury Strategies Expand to BTC, ETH, and SOL: Since April, MicroStrategy has added 24,000 BTC, while firms such as SharpLink and DeFi Development Corp have implemented ETH and SOL treasury strategies, aiming to optimize capital efficiency and shareholder returns. Bitcoin reserve strategies across more than 60 corporates have led to a 3% control of supply for this category of investor.

Infrastructure Adoption:

Stablecoins Enter Payment Rails: Global payments firms, including Visa, Mastercard, and Worldpay, rolled out stablecoin settlement capabilities that integrate with traditional systems while abstracting away blockchain complexity from the end user. This trend mirrors the early 2000s adoption of internet protocols, when corporates began leveraging online systems for operational efficiency without positioning themselves as technology firms.

Building Directly on Public Chains:

Asset Managers Tokenize Funds: Asset managers such as VanEck and BNP Paribas are operationalizing tokenization strategies to improve fund administration and collateral mobility. BlackRock’s recent engagement with DeFi protocols illustrates a shift from experimentation to full integration, where permissionless networks are viewed not merely as alternatives, but as complements to existing capital market infrastructure.

SEC Exploring Tokenization Pathways: The SEC is now reviewing frameworks that may ease security token issuance, opening a potential pathway for broader institutional participation in tokenized markets.

Global Brands Begin Building On-chain: International soccer league FIFA’s collaboration with Avalanche to build a dedicated Layer 1 blockchain for digital assets and fan engagement highlights how global brands are beginning to architect directly on-chain, similar to how media and retail firms transitioned from internet users to platform builders in the Web2 era.

005 Our Takeaways and Predictions

As we head into June, the crypto and broader capital markets are likely to remain active, defying typical summer seasonality. Last month was the strongest May for equities in over two decades and the busiest month for dealmaking in over two years. In crypto, headlines included Robinhood announcing its acquisition of WonderFi and completing its acquisition of Bitstamp, Circle renewing its IPO efforts, and Animoca Brands reportedly targeting a U.S. listing. Meanwhile, Anchorage Digital’s planned purchase of stablecoin issuer Mountain Protocol highlights growing consolidation around regulated crypto infrastructure. If this pace continues, public and private capital markets could become an increasingly important driver of crypto sentiment this summer.

Fixed-income markets remain a key variable to watch. Long-end Treasury yields rose sharply through mid-to-late May before easing moderately, as credit rating concerns and fiscal sustainability came back into focus. The multi-trillion-dollar spending bill working its way through Congress could add more pressure on yields if passed. At the same time, uncertainty around the economic outlook remains elevated. While markets have been promised trade and fiscal clarity “soon,” shifting deadlines such as those around steel tariffs and inconsistent messaging have introduced two-sided risk. Any softness in upcoming economic data could influence the Fed’s path forward, keeping rate expectations volatile through the next FOMC meeting. Trade tensions have also reemerged as a risk factor: President Trump recently reversed his tone, calling Chinese leader Xi Jinping “VERY TOUGH, AND EXTREMELY HARD TO MAKE A DEAL WITH” on Truth Social. A more benign tariff outlook now looks increasingly unlikely, adding another layer of uncertainty heading into June.

Meanwhile, BTC’s long-term support base continues to strengthen. Corporate treasury strategies remain active, with more firms adding BTC to their balance sheets. Over 60 companies now hold approximately 3% of circulating supply, and Pakistan became the latest government to announce a strategic Bitcoin reserve. These strategic buys, combined with rising ETF inflows and deepening TradFi access, create a potentially stabilizing force for BTC price action, especially in an environment marked by geopolitical tension, fiscal imbalance, and declining confidence in sovereign debt.

Key Events to Watch:

June 9: SEC Crypto Task Force Roundtable – DeFi and the American Spirit

June 18: FOMC

June 20: Quadruple Witching Day

Key Macroeconomic Data Releases:

June 11: CPI

June 12: PPI

To learn more about the topics covered in this month's newsletter, contact our team or reach out to your Galaxy representative.

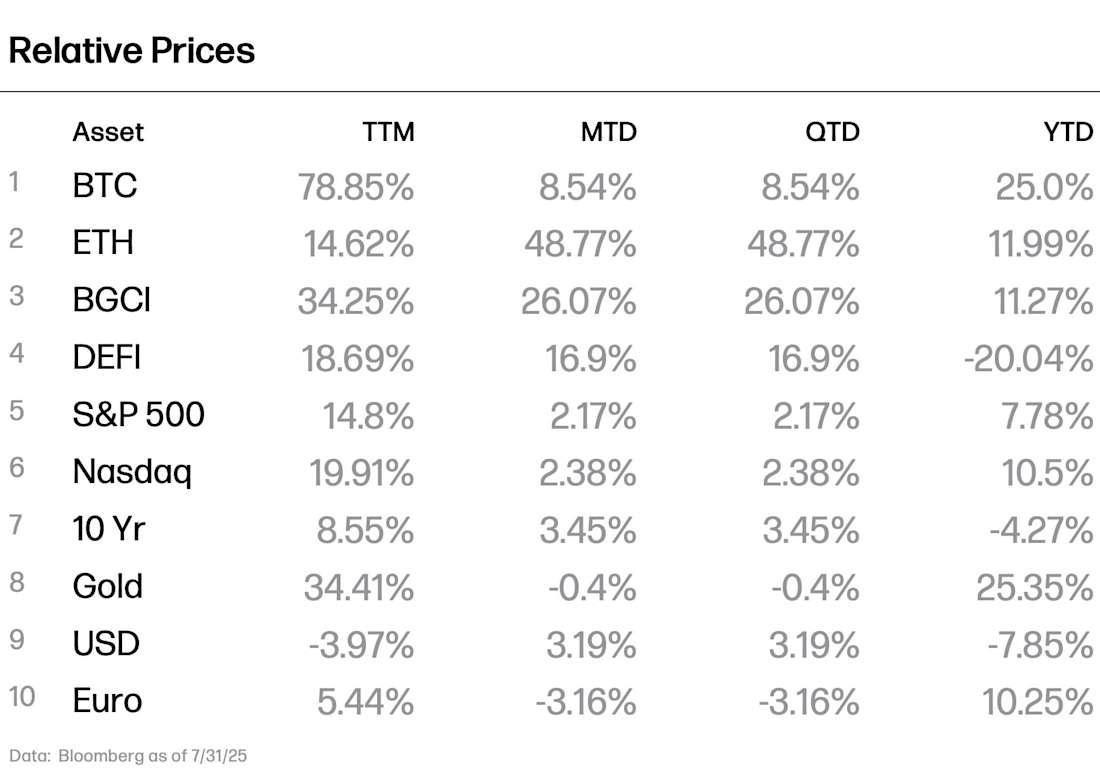

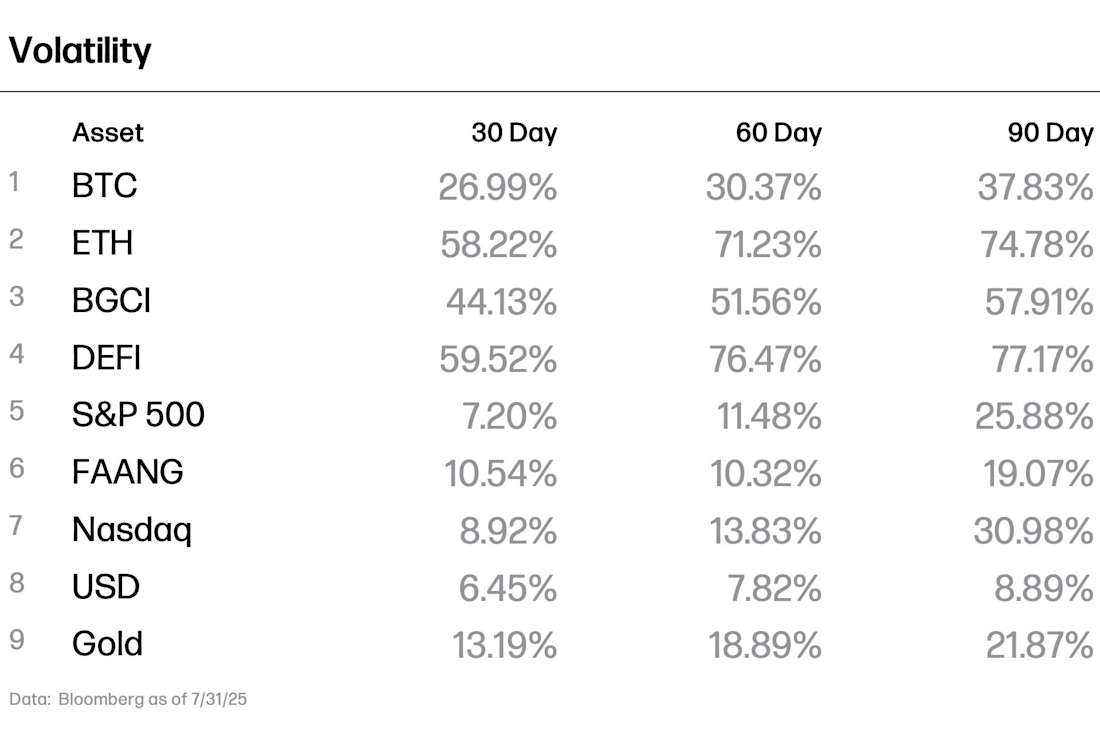

Crypto Performance & Volatility Data