January 9, 2024

Market Commentary

As we look back on 2023, the outlook on digital assets is much rosier today than a year ago. Operation Chokepoint 2.0 and the FTX trial, headlines that dominated the industry for a significant portion of the calendar year, have faded into the background as more promising times await crypto in 2024.

Digital assets concluded the year in strong fashion, with December appreciations for BTC (+13.57%), ETH (+15.75%), and the Bloomberg Galaxy Crypto Index (+24.91%). While the year’s final month is often considered a quiet trading period on Wall Street, December brought renewed crypto exchange volume not seen since the fall of 2022. According to The Block, monthly crypto exchange trading volume exceeded $1T for the first time all year in December, an indication of market strength as we head into the new year. This is the highest level since May 2022, another signal that market sentiment has now recovered from the Terra-Luna collapse which transpired that month. Putting a bow on 2023, digital asset funds saw $2.25B of annual inflows, a 2.7x YoY improvement. Beyond just leaving behind 2022’s tumultuous year for the industry, 2023 will go down as a top-three all-time year in terms of inflows for the asset class.

For the first time in recent memory, the digital assets rally in 2023 was spearheaded by the maiden cryptocurrency. According to CoinShares, Bitcoin accounted for 87% of all digital asset inflows, with $1.9B shifting into the market-leading cryptocurrency. The 2023 inflows illustrate an improving outlook for bitcoin as it had never before surpassed 80% of flows in a given year. Overall, bitcoin increased +159.22% during 2023, with it entering the top 10 for assets by market cap in December after eclipsing both Berkshire Hathaway and Tesla.

2023 also proved to be a positive year for bitcoin with regards to growing its user base, expanding the original blockchain’s utility, and ensuring the continued security of the network. This past year the number of bitcoin addresses with nominal balances surmounted 50M for the first time, serving as a proxy for growing global bitcoin adoption. While the Bitcoin blockchain has historically been viewed as possessing less functionality than some of its peer smart contract networks such as Ethereum and Solana, the introduction of the Ordinals protocol has expanded Bitcoin’s use cases beyond a store of value and peer-to-peer payments. During December, Bitcoin NFT sales totaled $853M, growing 127.64% month-over-month. Stemming from the Ordinals demand, Bitcoin transaction fees rose to their highest on record and topped the list of all blockchains with market caps exceeding $100M during a 7-day period in December. With the next Bitcoin halving on the horizon, transaction fees will become more vital in ensuring miners generate sustainable revenue to remain operational and provide the requisite hash power to secure the Bitcoin network.

Additionally, over the course of December, MicroStrategy furthered its bitcoin accumulation. In the last month, Michael Saylor’s company purchased another 14,620 bitcoins at an average price of ~$42,110. As of year-end, MicroStrategy’s bitcoin holdings exceed $8B. With the bitcoin spot ETF “Cointucky Derby” kicking off January 3, the positive sentiment regarding bitcoin will hopefully persist and continue attracting mainstream interest towards digital assets.

With bitcoin currently dominating the media’s focus on digital assets, several altcoins delivered strong December outperformances. As gas fees on Ethereum reached prohibitive levels, interest in Solana boomed as its token price swelled +72.33% in the last month. Other motivations behind Solana’s price rise include inflows of institutional capital into SOL-based funds and airdrops on the blockchain. The airdrop of Jito’s liquid staking protocol token resulted in the total value locked on Solana almost doubling to $1.2B in December (the Jito liquid staking protocol is intended to be the Solana equivalent of Ethereum’s Lido protocol). Another Solana token, a memecoin called BONK, surged 232% in December, augmented by its listing on Coinbase’s exchange.

Portfolio Considerations

As we embark on the journey into 2024, it's imperative for investors to navigate the ever-evolving crypto landscape with foresight and strategy in mind. In this section, we'll delve into several key portfolio considerations.

Considering the challenges faced by the crypto industry in 2022, the past year’s price performance exceeded many expectations. Looking ahead, three significant events loom. First, the anticipation of a spot BTC ETF—which drove much of bitcoin's price performance in 2023—has been greater than ever. It is expected that an SEC approval may occur any day now and is expected to potentially lead to substantial net new inflows into bitcoin. Second, the Bitcoin halving, as we’ve mentioned in previous newsletters, will occur for the fourth time in April. Third, potential interest rate cuts by the Federal Reserve should help set the stage for a promising year for the crypto space.

For Ethereum, the anticipation of a potential spot BTC ETF suggests continued upward momentum for ETH during the ETF application process. Upon approval of spot BTC ETFs, spot ETH ETFs are likely to follow suit, then offering an ETHBTC trading opportunity. In fact, Ethereum's relative underperformance began showing signs of reversal in December. Furthermore, Ethereum developers are intensifying their testing efforts for the forthcoming Dencun upgrade, scheduled for this year. This upgrade introduces "proto-danksharding," enhancing data storage capacity and reducing fees for layer 2 rollups, making ETH more competitive with Layer 1’s like Solana. The Goerli test network is set to implement Dencun on January 17, marking a significant milestone. With a 90% 2023 return for ETH compared to SOL's 940%, there's a favorable risk-reward profile for Ethereum. Finally, there is a lot of excitement around Eigenlayer and restaking. As this sector develops, ETH staking rates are expected to rise, increasing demand for the token.

While 2023 brought substantial price gains, it also featured ongoing legal and regulatory actions, including battles between the SEC and entities like Ripple, Grayscale, Binance, and Coinbase. The SEC's authority in the crypto space faced setbacks, raising questions about its credibility. While regulatory overreach remains a concern, our inability to effectively self-regulate underscores the necessity of government intervention to address challenges within the crypto space. Enforcement actions against major crypto companies, the government's role in cleaning up the industry, and the regulatory landscape will continue to be prominent themes in 2024. Some regulatory headwinds to be aware of are the impending election season, potential continued opposition from SEC Chair Gary Gensler, and concerns among lawmakers about the scope of proposed bills. These bills aim to regulate stablecoins at the federal level and address crypto market structure broadly. Despite passing the House Financial Services committee in July, their progression to the Senate Banking Committee remains uncertain. As USV’s Fred Wilson puts it, “Innovation never waits for rules and regulations. But it eventually gets them.”

Institutional Adoption Highlights

Michael Saylor plans to sell $216M worth of MicroStrategy shares to buy more BTC.

Deloitte taps Polkadot ecosystem’s Kilt blockchain to improve shipping logistics.

Deutsche Bank’s asset manager arm DWS joins Galaxy to issue Euro stablecoin.

FIFA is launching NFTs that give holders a chance to secure World Cup finals tickets.

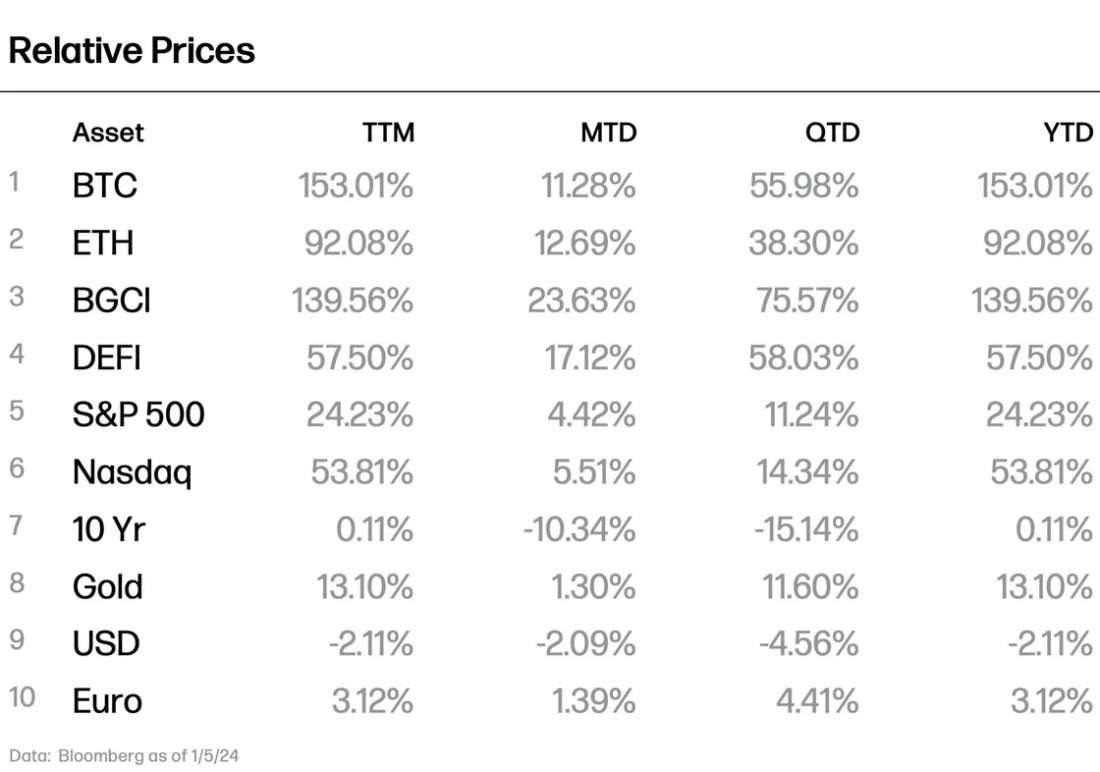

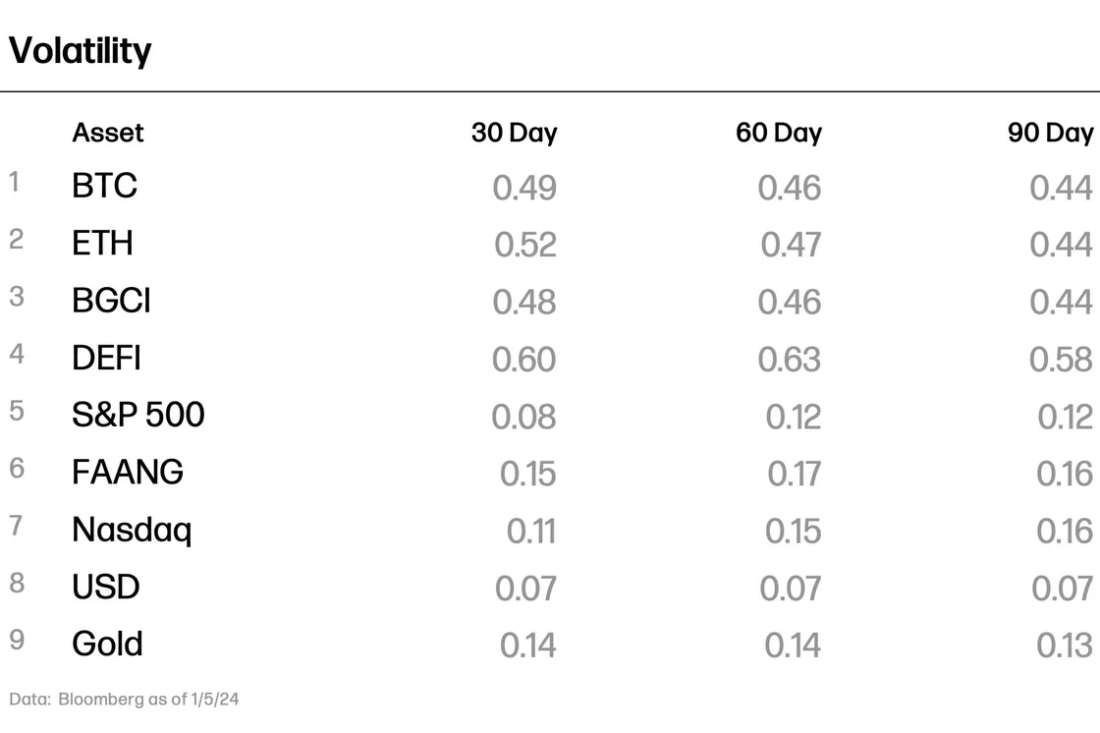

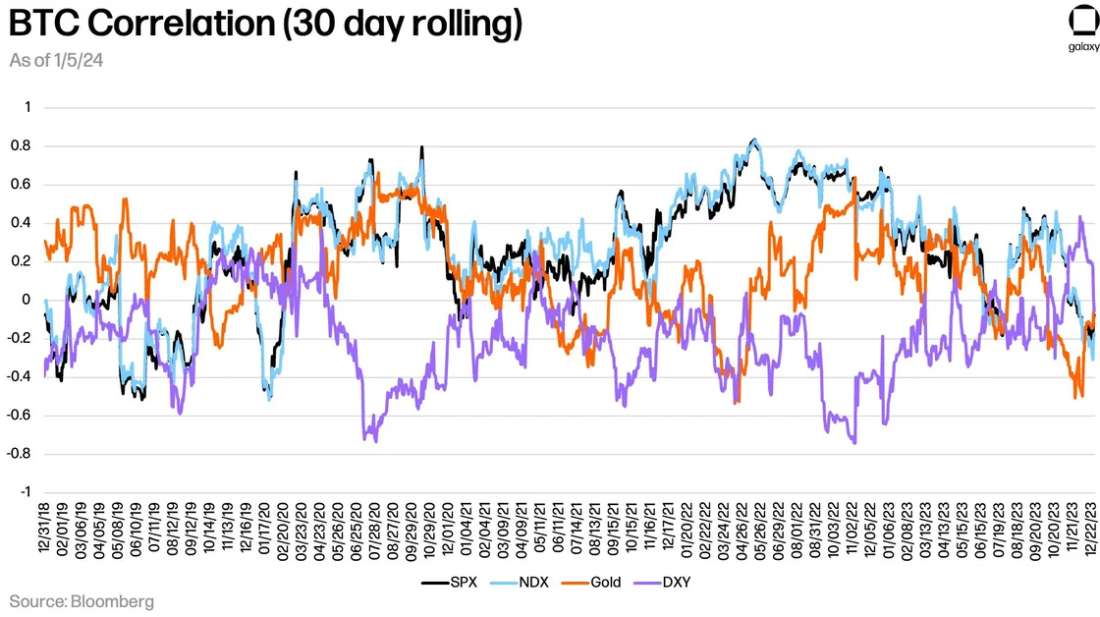

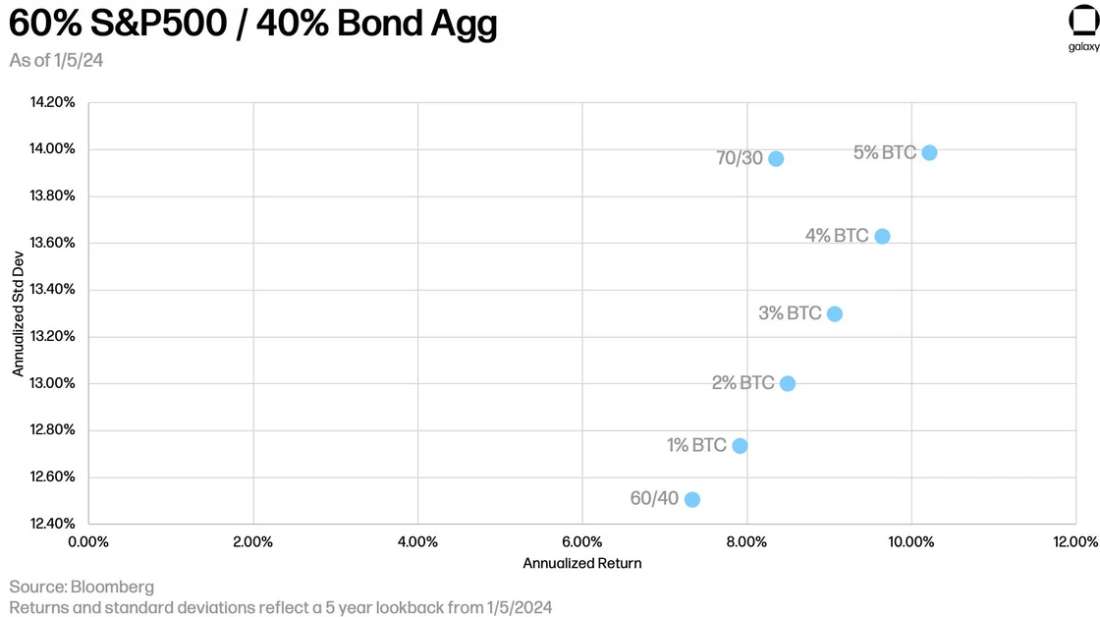

Crypto Performance and Volatility Data